Do you need to travel outside the US this April? Are you short on time to file your federal tax returns? Then it would be a good idea to file a personal tax extension with the IRS. If you are an Indian in the US who is unsure to file a personal tax extension, we can help you.

Our easy 8-step guide will walk you through the process on how to file a tax extension in eight easy steps.

But, first things first.

What Is Personal Tax Extension Form 4868?

The deadline to file federal taxes in the United States is April 15. However, many people are unable to meet the deadline due to various reasons. In this scenario, one can fill out Form 4868 to file a personal tax extension. However, you have to submit this form to the IRS (Internal Revenue Services) before the due date. This will let you avail a six months extension till October 17 to file your income tax returns (ITR).

However, this extension is on filing the ITR and not on the tax payment. You will be required to make the income tax payment by April 15. Failing to do so will attract penalties. Moreover, this form is to be filled by individuals and not by businesses or corporations.

Form 4868 is available on the IRS website. You will need the following details to complete the form:

Your social security number (and your spouse’s too if filing a joint return)

Address

Estimate of tax liability for the year

Taxes already paid (tax withheld by an employer)

Calculation of deductions and credits

Where to file?

Filing a personal tax extension is easy, free, and convenient. One can file it electronically on the IRS website. Or print a form from the website, fill in the requisite details and mail it to the IRS directly.

How To File A Personal Tax Extension?

Filing a personal tax extension may sound more difficult than it is. But it is convenient if done before the due date. Here is a guide to help you file a personal tax extension:

1. Electronically

You can use IRS Free-file (IRS Free File | Internal Revenue Service)to file a personal tax extension via form 4868. Once you fill in the required information and make the tax payment, you will receive an acknowledgment from the IRS. Keep it as a record to submit it in October when you file your returns. One can use Free File to file form 4868 if their adjusted gross income is under $73,000 for the last financial year. If your income is above the threshold, opt for the IRS Fillable Forms tool(Free File Fillable Forms | Internal Revenue Service (irs.gov) to file for a personal extension. Your tax preparer can also help you with it.

2. Mailing A Tax Extension Request

If you are planning to send your request for a personal tax extension by mail, print form 4868 from the IRS website. You can also get the form from your local post office or the IRS.

Fill in the details, attach your tax payment check, and mail it to the IRS. Snail mail takes time, so rather than waiting until April, do it now.

3. Tax Payment

Form 4868 buys you more time to file your taxes. However, this does not defer your payment till October. One is required to pay their dues by April 15. Hence, you can pay a portion or all of your taxes online through a debit or credit card, or DirectPay. You can also mail a check or send a money order to the ‘United States Treasury’ along with your form 4868.

4. Special Tax Payment Extensions

Certain individuals get an automatic 60 days extension on filing and payment of their ITR. These are citizens or resident aliens of the United States who live outside of the United States or Puerto Rico. They could be serving in the military or on the naval outside of the United States or Puerto Rico.

Similarly, those in the Armed forces working in combat zones in or outside the US also get 180 days tax payment extension. All the above-mentioned individuals should explain the reason for the delay when they file their returns. However, if you owe taxes to the IRS by the due date, be prepared to pay the interest on the amount accrued.

5. Tax Extension Approval

If you apply for a tax extension online, you will receive confirmation within 24 hours. However, you may need to phone the IRS office to see if your request has been received if you’ve sent it via snail mail. The IRS will usually allow you an extension unless there is a problem with your form. And will not contact you unless there is a problem with your form.Also, you will not be contacted by the IRS if you have filled the form properly.

6. Tax Payment Options

If you can’t pay your taxes in full by the April deadline, you can choose to pay them in installments. The IRS’s website allows you to select a payment plan.

7. Tax Relief Options

If you require tax relief due to financial difficulty, you must file Form 843 (Form 843 (Rev. August 2011) (irs.gov). The same holds if you haven’t paid your taxes in a while or if the IRS has given you incorrect written advice. You can file an appeal if they reject your request.

8. State Tax Extensions

The above method is applicable for federal tax extensions. Some states offer a six-month automatic personal tax extension, while others do not collect state taxes at all. For more information, get in touch with the appropriate state officials.

It is easier to file a personal tax extension if the preceding steps are followed. Do not, however, use it as an excuse to pay your taxes late. You’ll get in trouble with the IRS and face a penalty if you do.

Are you still skeptical about filing a personal tax extension yourself? Then we are here to help you out. Use the services of AOTAX to remain on top of your tax deadlines. Over 2 lac Indians have benefited from our team of skilled tax consultants and planners who have helped them submit their US taxes on time.

December is the holiday season and the perfect time for giving gifts. It is the time when your employer might even plan about giving bonuses to you. This would reflect a sense of gratitude towards you for the good services you have provided across the year. When you come across the news that you would be receiving a bonus this holiday season, it’s obvious for you to make certain plans about how to spend your extra income you receive.

However, you must remember that the holiday bonuses you receive would be considered as compensation exactly in the same way as that of your salary paychecks. So, taxes would be withheld from the holiday bonus you receive.

Now, let us have an idea on how and in which way the holiday bonus you receive would be taxed.

Social Security Tax

In the year 2020, you would have to pay Social Security tax on all the compensation you have received up to $137,700.However, if you have not reached up to that limit, and then your employer would deduct around 6.20% from the bonus you would obtain for the purpose of Social Security.

Federal Income Tax

When you are receiving your bonus and it is an additional income for you, then the IRS would definitely withhold a flat percentage from your bonus. Earlier, the federal income tax rate which would be withheld on the bonus was 25% which has been reduced to 22% now. Moreover, your employer can combine your salary and bonus and then withhold the taxes from the entire amount. This would be much higher than 22% but you should be assured that the money which has been withheld would not be lost. The tax rates on your bonus would be much higher than the actual tax rate levied on the total income you have earned. So, while filing your tax returns you would get back some of the amounts as your federal tax return.

Medicare Tax

You would be paying Medicare taxes on all the compensation that you have received and hence, another 1.45% would be deducted in the form of Medicare Tax.

State Income Tax

Most of the states would impose Income Tax separately on the bonus that you have received. So, the State Income Tax would be withheld at the same rate as determined by the State Law.

Contributions towards Retirement Plan

In case, you have decided along with your employer to withhold a particular percentage from your salary as a contribution made towards your retirement plans such as a 401(k)plan or any other plan then it would be withheld from your supplemental income or bonus.

For example, if you and your employer have decided together on the withholding of 15% from your salary towards your retirement plan then 15% would be withheld from your bonus currently. So, this might be harder on your finances as of now but it will help in having a larger fund for your future after you retire.

So, now by adding all this resulting amount would be deducted together from your supplemental income/bonus. However, you must keep in your mind that today you would be obtaining the bonus and you can even get some amount back in the form of a tax refund

Conclusion

Hence, if you are having some supplemental income in the form of a bonus then you are supposed to pay taxes on them.

What to do if you have missed your Tax Extension deadline?

Due to the poor economic conditions caused by the pandemic COVID-19, the US Government had extended the tax filing deadline for the Americans due on 15th April 2020 to 15th July 2020. However, millions of Americans have not been able to file their tax returns by the 15th of July 2020 and have filed for an extension. By this extension, the tax return filing deadline would be extended up to 15th October 2020 which has even passed now.

So, if you have missed your extended tax return filing deadline then you might be wondering about certain factors. Let us have a look at what are the common things to be considered if you have missed your extended tax filing deadline.

Should you still file your tax returns if you have missed the extended deadline?

Yes, even if you have missed your extended tax return filing deadline you must file your tax returns soon. You must fill your tax returns even if your income level was lower than the minimum income level set by the IRS i.e. $12,200 when you are filing your tax returns as a single individual and $24,400 in case if you are married and are filing your tax returns jointly for the year 2019. You must also file your tax returns even if you are eligible for availing credit like Earned Income Tax Credit.

The sooner you are going to file your tax returns; the penalties you would pay for missing the extended tax deadline would be less.

What would happen if you miss filing tax returns by the extended deadline?

If you are going to obtain tax refunds from the IRS, then you would not be paying any penalty for missing your extended tax filing deadline. But, if you missed your extended tax deadline and have taxes due to pay to the IRS then you would have to pay penalties. Usually, this penalty is 5% of the tax that has not been paid and varies up to 25%. This penalty is calculated at the beginning of each month for which the tax has not been paid yet.

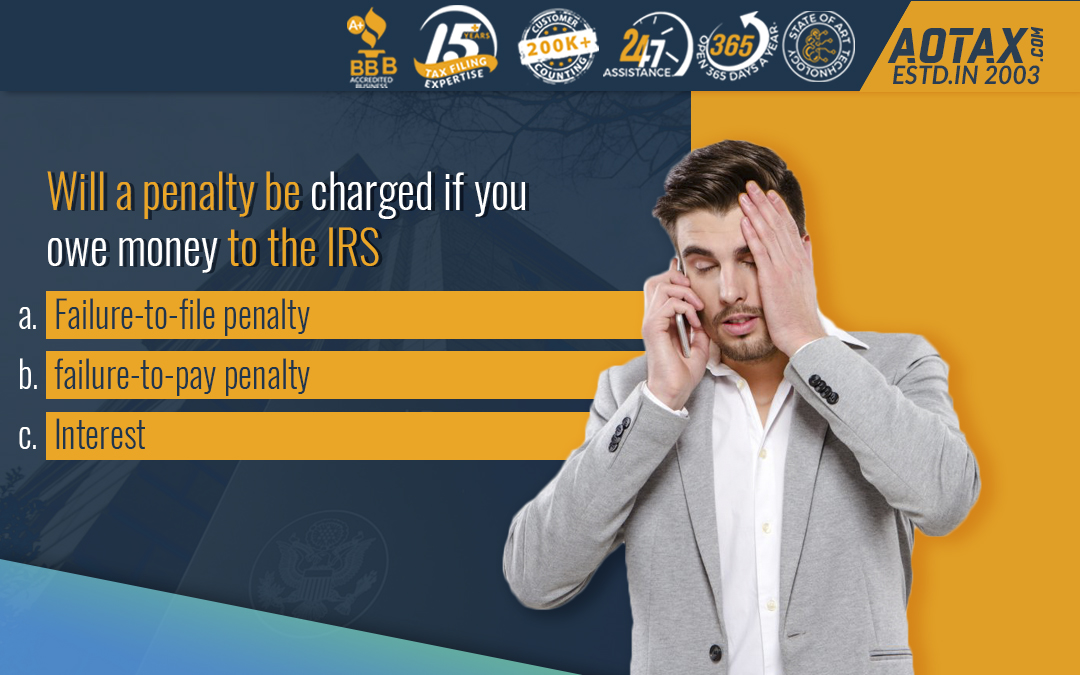

Will a penalty be charged if you owe money to the IRS?

If you owe money to the IRS, then there would be three types of penalties which you would have to pay.

Failure-to-file penalty.

This penalty would be charged if you are not able to file your tax returns on time. This failure to pay the penalty would be applicable for a full month or for a specific part of the month for which the return filing has been delayed.

Failure-to-pay penalty.

If you have not been able to pay your taxes to the IRS on time, then the IRS would impose a penalty. This penalty would be around 0.5% of the tax that is due to be paid to the IRS.

Interest.Interest would be charged by the IRS if you are not able to file your tax returns on time or pay your taxes according to the due dates.

Will you still be paying penalties if miss the extended deadline due to financial hardships.

With the havoc created by the pandemic COVID-19, it is quite obvious for you to be facing economic hardships. However, if you can state the reasonable cause behind the inability to file tax returns or inability to pay your taxes your penalties might be relaxed.

In case, you have been affected by the natural disaster which has been declared by the Federal Government then you would obtain relief while paying the taxes or filing the tax returns.

So, even if you have missed your extended tax filing deadline you should not forget completely about filing tax returns.

Repayment of debts can give you nightmares and this entire problem is a vicious circle. With one debt leading to another, the entire process can push you into financial troubles.

So, it is essential to get rid of your debts soon; however, it seems to be a difficult thing if done without prior planning.

Let us check out a simple guide which would help you to get debt-free this year.

The Essentials

It’s a consumer world today and it’s the current trend to purchase new and fancy items. You might be having the best of clothes, apparel, and gadgets but you are interested in upgrading them. Expansion of your wardrobe has become a hobby and a passion too.

Let’s think rationally and put an end to this. It is necessary that you prepare a list of the essential items and only purchase those which are needed. Avoiding unnecessary purchase is the best way to minimize your expenses thus, leading to less debt accumulation.

Budgeting and tracking your expenses

Budgeting is highly essential to keep your finances under control. When you make a budget, know your expenses, and spend accordingly you would be able to save. These savings can be your savior while you are struggling to get rid of your debts. There are various budgeting tools and apps available that can be utilized to keep a check on your income and spending. When you are aware of your spending habit, you can easily find out those areas where you can cut off the spending. The cut-off spending would be used in paying off debts.

Search for shopping options which are cheaper

When you are trying to have a debt-free life, it is essential to introduce some changes to your shopping options. You can resort to techniques like shopping in bulk. This would be less expensive. Moreover, for the general household shopping, you can plan to visit the stores once during the month. Your shopping list for essential items would help you in obtaining all the necessary items at once without the need for visiting the stores and also spending again and again.

If you fill up your cupboards with the groceries, stationeries and other items when they are on sale and then skip shopping each month for at least 1-2 months, you would be able to save quite a good amount. The savings made can be utilized in making your debt payment then you would get rid of your debts in a considerable period.

Handle your credit card wisely

You can consider your credit card as a source of cash that would be needed at times of emergency. But, if you are making improper use of your credit card you might be accumulating debts. You should ensure that your credit card is used only in times of emergency. Avoid making payments by using your credit card; rather plan the purchase of items only when you have cash with yourself.

You should keep on checking the records of your credit card continuously. This would help you in keeping a track of how much debt you have to pay off. Moreover, you must be aware of any fraud schemes which can occur with your credit card. Also, if you feel that the interest rates of your credit card are too high you can negotiate with your card issuer. If you have had a good history of paying your bills on time then you can expect getting a lower interest rate.

Make extra money

If you decided to get rid of your debts this year, then you must find out other methods to increase your income. You can take up an extra job or work in extra shifts, putting all extra money earned into the debt payment. Once your debts are paid off, you can stop doing this extra work if it is painful for you. Moreover, you can rent out your extra space such as a garage, or room, etc. and use the extra income for paying off your debts.

Get rid of the expensive debts first

This is one of the smartest methods to use for getting rid of the debts which you have. You must choose one of those debts of yours which are charging the highest interest. All the extra payments you can do must be focused on getting rid of this expensive debt first.

Once your expensive debts are paid off, utilize all the money that you were paying for that particular debt in paying off the next expensive debt of yours. By continuing this method, you would be able to pay off all the debts and would be left with the least expensive ones only. You would feel motivated by using this strategy as it helps you in getting rid of the debts quickly.

However, there is another strategy too i.e. the Snowball Method which is a variation of this method and is also helpful in getting rid of debts easily.

Refinancing

The idea of refinancing your present debts would be of great help in paying off your debts. Several loans come up with attractive rates of interest. Getting that money and using it for paying off your debts would be a good strategy indeed. However, you need to be careful and consider the opportunities cautiously while refinancing.

Do not accumulate debts

The golden rule to become debt-free is to prevent the accumulation of further debts. This process is a vicious circle and it needs to stop. One of the best methods by which you can keep a check on your debt accumulation is by the restricted use of your credit card. Moreover, spending wisely by minimizing your expenses is the best method to stop any further accumulation of debts.

After you have stopped the further accumulation of debts, you can opt for the restructuring of your installments and payment strategy. By this, you would have a good financial strategy for your debt payment.

Conclusion

So, if you are interested in saving so that your debts are paid off you need to have a mindset change. You will have to think twice before shopping, make smart shopping decisions, and turn down temptations. With a substantial amount of self-control and discipline while dealing with finances you can easily get rid of your debts this year.

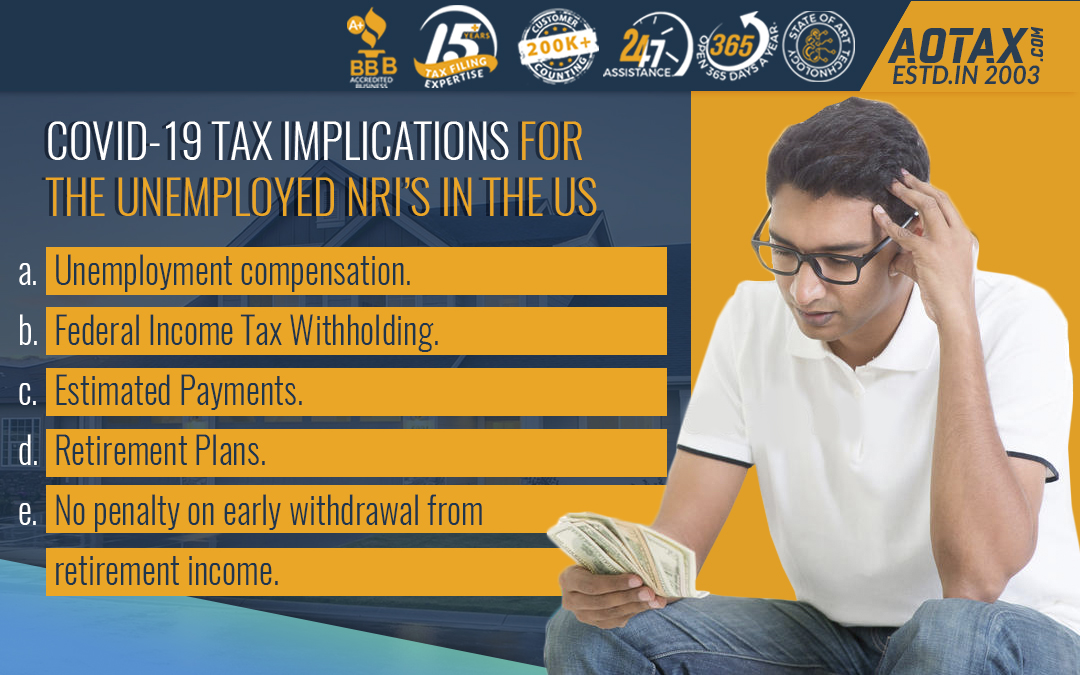

Covid-19 tax implications for the unemployed NRI’s in the US

The pandemic COVID-19 has led to a complete economic setback across the United States. Many businesses have been closed down some partially and some completely. Millions of Americans have become unemployed and are facing various financial crises. The US Government has provided various tax reforms to alleviate the economic stress faced by the Americans during these challenging times.

Let us talk about some of the major tax implications for the unemployed NRIs during this distressful COVID period.

Unemployment compensation

For Income Tax, the unemployment compensation offered is taxable. This would include the unemployment benefits obtained from State and the $600 which has been received from the Federal Government. You will have to inform us about this total amount received on Form 1099-G. You must spend your benefits after considering the consequences.

Federal Income Tax Withholding

To avoid surprises, you can opt to choose for Federal Income Tax Withholding from your unemployment benefits obtained during the year. This process would be almost similar to withholding on from your paycheck thus; you would owe less at the tax time.

Estimated Payments

You might be feeling that you would owe more at the tax time; to avoid this you can make estimated tax payments throughout the year. You can keep on making estimated tax payments throughout the year and thus, avoid a potential penalty. Moreover, the IRS has waived any penalty and interest on the tax payments which were due on 15th April 2020 which was later on extended to 15th July 2020.

Retirement Plans

Any withdrawal which you are making from your retirement plans or pension plans is considered to be taxable unless they are being transferred to an IRA. Under the provisions of the CARES Act, this tax is not due at once. You can make the payment of this tax in three years. You must check with a tax advisor if you are planning to make a withdrawal from your retirement plan as the taxability of the retirement income can be complicated.

No penalty on early withdrawal from retirement income

In general, there is a 10% early withdrawal penalty on making any withdrawal from your Retirement account before you reach the age of 59-1/2 years unless it is an exceptional case. However, this year you are eligible to withdraw up to $100,000 from your IRA or 401(k) plan without having to pay any penalty. But, you will have to pay Income Tax on the withdrawal you make in the form of Retirement Income or Accrued benefit.

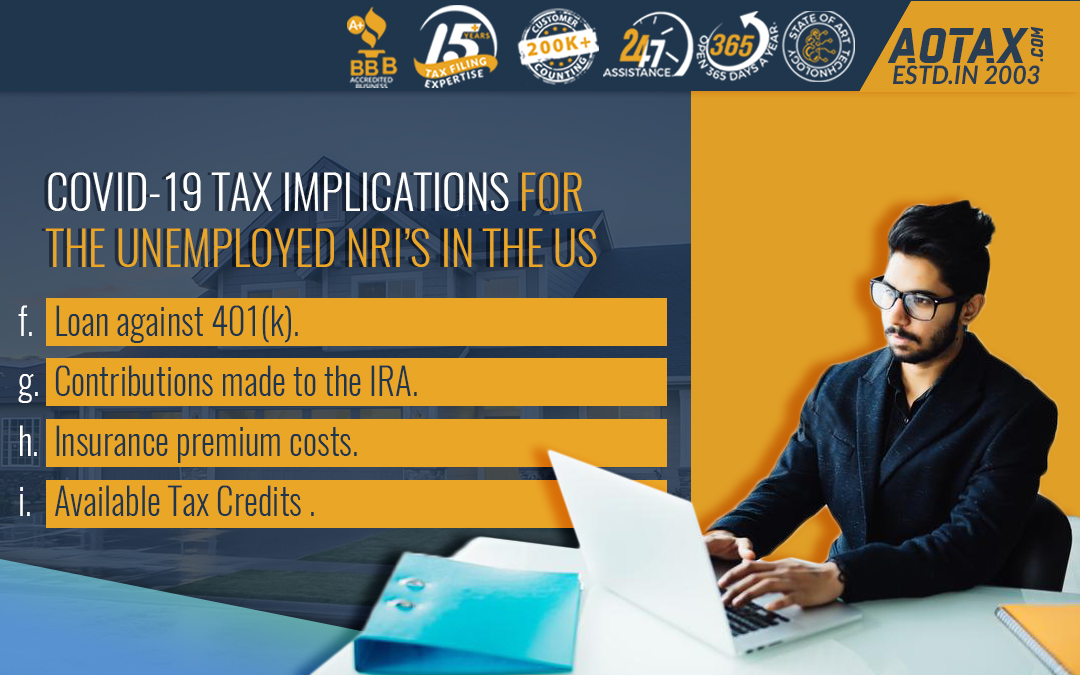

Loan against 401(k)

If you need extra cash, you can take a loan against your 401(k) plan. You would be able to borrow up to 100% of your account balance or $100,000, whichever is less. At the time of re-payment, you would be able to defer the payment and pay back the loan in five years without any taxes applied. However, you must check with the authorities before opting for this as the implications might vary for different plans.

Contributions made to the IRA

If you have made any contributions to your IRA and now to need the money back, you can avail of this benefit as well. The contributions made to the IRA if returned before your date of tax return filing can be withdrawn without paying any penalties. You are eligible to take out the contribution and any dividend which has been earned. However, even if you make the contribution back you will not be able to claim a deduction for the contribution made initially on your return.

Insurance premium costs

Now since you are unemployed, you will be responsible for making the payment of your health care costs. So, you are eligible to deduct the cost of the health insurance premiums including the COBRA costs as the Medical expenses. You can include the costs related to these premiums and other eligible medical expenses on Schedule A when you itemize your deductions. However, you should keep in mind that only those expenses are deductible which can exceed 10% of your AGI i.e. Adjusted Gross Income. Moreover, you can also use the money from your HSA (Health Savings Account) for making the payment of the medical expenses. Even if you lose your job, the money present in the HSA is yours.

Available Tax Credits

You should not overlook those credits for which you had not qualified when you were employed. In the previous years, your income might have exceeded the threshold for the Earned Income Tax Credit (EITC) but you would be eligible to avail the credit now. If you meet the Earned Income Restrictions and other criteria now you can obtain the credit.

Conclusion

So, even if you are unemployed there are several methods by which you can avail of certain benefits, credits. You must resolve any queries which you have about the credits and deductions so that the tax which you owe can be reduced.

Step-by-step guideline on what to do if you cannot afford to pay your taxes

The IRS had extended the tax return filing and payment deadline until 15th July 2020 for the Americans to alleviate the financial crisis faced by millions of Americans due to the pandemic COVID-19. However, the pandemic has led to the unemployment of millions and millions of Americans. So, even with the extension in the return filing and tax payment deadlines, it is quite difficult for some Americans to pay their taxes on time.

The IRS has a simple reminder for the taxpayers who cannot pay their entire amount of federal taxes which they owe. They should file their tax returns on time and pay as much as possible. By this, the interest and penalties of taxpayers would reduce and there would not be much accumulation of interest to pay back.

If a taxpayer plans to pay his taxes as much as he can afford, then the IRS has some convenient methods to do this i.e. by IRS Direct Pay Method, Electronic Federal Tax Payment System (EFTPS), Electronic Funds Withdrawal, Debit or Credit card, or by Check/Money Order, etc.

However, for those taxpayers who feel payment of taxes are unaffordable at the moment; they can follow a detailed plan.

Step1 – File by the new 15th July deadline even if it feels difficult to afford the payment on time

As said earlier, due to the pandemic COVID-19 the deadline to pay the Federal taxes has been pushed to 15th July 2020. However, with this extra time, taxpayers should not wait much more to file their taxes. Taxpayers must consult tax professionals for filling the forms. By this, the credits and deductions to lower the bill can be found out easily.

Many taxpayers might consider the option of the deadline extension. However, the extension would provide more time for filing the tax returns but not for

paying the taxes. Even if there is an extension, the tax payment must be done on time. So, an extension should only be filed by the taxpayers if due to some reason the taxpayer is not able to file the tax returns on time.

Step2 – Pay as much as possible by the tax deadline

This is also recommended by the IRS that the taxpayers should wait till the deadline, try to arrange for the tax amount, and pay off as much as possible. Some taxpayers even prefer discarding some of their unwanted materials in exchange for cash which can be utilized in payment of their taxes which are due.

Taxpayers can contact the IRS on the toll-free number to discuss alternate payment options. IRS might help the defaulter taxpayers with other payment options like a short-term extension to pay the taxes, an

agreement for installment, an offer in compromise, or by temporary delay in the collection by reporting that the taxpayer’s account is currently not collectible until the taxpayers can afford to make the payment.

Step3 – Keep paying the taxes you owe even after filing

Even after Tax Day, taxpayers would have a period of around 1 month or 2 months before the IRS would contact them about the rest of the tax payment. During this available time of 1month or 2 months, taxpayers should try to pay out as much as possible to reduce the balance left out.

In case the taxpayers are not able to make their complete payment by this time, the IRS would suggest options for making the rest of the payments in monthly installments.

Step4 – Rectify the problem

You should approach a tax professional and try to work with him or his team to ensure that you are not stuck with the problem of unaffordability related to tax payments. This can be feasible either by setting aside profits from a side business or by the adjustment of withholdings from your paychecks.

Your issues can be best identified and rectified by the tax professionals so that these issues are avoided in the future.

Conclusion

Hence, you can follow these steps and try to pay off as much tax as you can. Avoiding the aggregation of penalties is important to avoid any further financial and economic hardships.

Recent Comments