Tax filing season is arguably the most nerve-wracking time: battling documents, figures, and important dates is an all-consuming task. In addition, filing your taxes demands a constant awareness of your finances, tax strategy, and IRS regulations.

A change in one could significantly impact the rest, and this is undoubtedly true for changes that the Internal Revenue Service (IRS) often implements through tax season.

Changes in laws, policies and tax forms can throw your preparation off track. Unfortunately, we’ve seen multiple instances of the same over the last few years due to Covid-19 and the bills passed to alleviate its effects.

However beneficial or necessary, these changes leave taxpayers like you scratching their heads while trying to make sense of these amendments and additions.

No one likes to be caught off-guard, and certainly even less so by the IRS. So we’ve compiled a list of changes you can expect to see on this year’s forms, so you can be prepared to optimize your tax bills.

So, What’s New This Year in Personal Income Tax Return?

Taxpayers can expect to see various changes on their tax forms for the last financial year, especially regarding deductions and credits. Keep reading to know more.

Form 1040 and its schedules

This year’s Form 1040 is far from compact, with Schedules 1,2, and 3 all having expanded to take up close to two pages each. This elongation is due to additions to income and extra taxes, each getting their sections instead of being grouped into one confusing bundle. Additionally, there are many changes related to credits and deductions that we’ll discuss below in more detail.

Lines 19 and 28 on Page 2 of Form 1040 were adjusted to account for changes made to the credit and consider that it was fully refundable for 2021.

Earlier, the credit was only partially refundable (up to $1,400 per child) and was only applicable for children 16 years and younger (now, parents can claim the credit for 17-year-olds).

Earned income tax credits

The Earned Income Tax Credit was upgraded due to changes in the American Rescue Plan Act. Most importantly, the Credit now allows more childless taxpayers to claim the credit.

The age limit has also been increased to allow people aged 19 to 65 to claim the credit on their 2021 tax returns. Line 27 of Form 1040 has been modified and expanded to accommodate these changes.

Recovery rebate credits

In 2020, the Recovery Rebate Credit on Form 1040 was meant for people who didn’t receive their first and/or second check or those who received an incorrect amount.

For 2021 however, it must be noted that the credit is only for those who did not receive their third check or for those who didn’t receive the entire amount. Therefore, taxpayers must lower their credit claims to account for this.

Savers credits

The Savers Credit aims to encourage lower and middle-income taxpayers to save for their retirements. The credit was allowed for 10%, 20%, or 50% of the first $2000 saved, depending on income and filing status. However, for the 2021 tax return, taxpayers can claim a 50% credit if their AGI is $19,750 or less. Form 1040 considers this.

Deductions

Standard deductions

Due to adjustments for inflation, the deductions that taxpayers can claim are much higher and are reflected on your tax forms. The increments to the 2020 amounts are as follows:

$300 extra for married couples filing jointly

$1,350 per spouse for couples over the age of 65

$150 extra for single filers, $200 for those over 65

$150 for head-of-household filers

Charitable deductions

Earlier, deductions claimed for any charitable donations would affect taxpayers’ AGIs. This is no longer the case, and the space allowing you to check the $300 charitable contribution option has been moved elsewhere in the form.

Additionally, married couples can now individually claim deductions instead of being counted as one entity. That means that married couples can claim up to $600 in deductions for donations.

Tax brackets

The tax brackets from 2020 remain the same, but the income ranges that fall into them change. This determines the amount of tax you pay, so check where you fall wisely.

You can then appropriately complete line 15 on Form 1040 pertaining to taxable income.

Taxes for the self-employed

The tax breaks that self-employed taxpayers can take have been tweaked and include:

Deductions of up to 100% for business meals (to be claimed on Line 24b, Schedule C).

Long-term care insurance premiums do not have to be itemized and can be deducted on Line 17, Schedule 1.

Unemployment benefits

An unemployment compensation benefit worth $10,200 was in effect from 2020 but no longer. Therefore, any compensation earned in 2021 will be fully taxed in the upcoming tax return season. The same must be mentioned on Line 7, Schedule 1 of Form 1040.

Student loan discharges

Students with undergraduate and graduate student loans no longer worry about the forgiven student debt being a part of their taxable income. Earlier, this amount had to report on Line 8c, Schedule 1, but now this can be left blank.

Next Steps

The best thing taxpayers can do at the moment is to take stock of how these changes affect their filing statuses and strategies and then prepare their documents accordingly.

However, the complexity of filing your taxes cannot be understated, and often the best thing to do is to hire a tax professional to help. With close to two decades of helping Indians in the US prepare for, and file their tax returns, AOTAX is the best. We can help you get everything in order and ensure that your tax forms are error-free. Sign up for free today!

Is a complete understanding of the US taxation system still eluding you?

Does the complexity and endlessness of IRS forms overwhelm you?

Well, we’re here to tell you that you are not alone.

Thousands of Indian IT professionals embark to America for better pay and jobs and often get caught up in the confusing web of filing their tax returns.

A new country and different laws can complicate tax season, but you can better handle it with some preparation and organization. So we’ve come up with the ultimate checklist to help you prepare for filing your taxes.

What are the Documents Required for Income Tax Return of Individuals?

Depending on your financial and personal context, the claims you make while filing your tax returns can vary. Therefore, multiple documents are often required, which can be hard to track.

Nevertheless, we’ve categorized the documents required for income tax return of individual per the functions they serve while filing your taxes. Read on to know exactly what you need to keep handy to sail through the tax season smoothly:

Personal Information and Dependent Information

Basic identification information is mandatory while filing tax returns. Be sure to include the following documents:

Previous tax returns and statements for reference. The IRS has up to three years to decide on whether to audit an individual or not. In such a scenario, having copies of previous tax returns is necessary to ensure the best outcome.

Social Security or Tax ID numbers and dates of birth of both you and your dependents, if any. Dependents include spouses, children, parents whom you provide for financially. In the case of child dependents, furnishing childcare records is advisable.

Income-Related Documentation

Your total income determines your tax bracket and how much tax you pay. However, you are legally required to file taxes for all the types of income you receive, including rental income, interest on investments, and profits made on anything you choose to sell in the year.

In addition, the US Government taxes Indian H1B holders on their global income and their US income. Therefore, you must declare any profit-generating assets back in India as a part of your income. It is advisable to keep the documents below ready and submit them as a part of your tax return:

Form W-2: issued by your employer and states precisely how much tax was withheld from your pay.

Form 1099 series: each form in this series has a different suffix to indicate the different types of revenues possible:

1099-INT: for income in the form of interest earned on investments.

1099-G: for government payments and tax refunds.

1099-K and 1099-MISC: for payments received for freelance gigs.

1099-R: for pension income.

1099-S: for income received upon the sale of stocks.

1099-B: for income received after selling a property.

1099-DIV: for dividends received for mutual fund investments.

1099-SSA: for Social Security benefits.

Form 1040: to be used while declaring foreign income and reporting taxes paid in previous years.

Cryptocurrency transaction records of sales, if any, and interest earned.

Form 1095-A: for Health Insurance Marketplace Statements.

Rental asset records: for income earned in the form of rent.

Expense records: bank and credit card statements.

Form W-4: for changing the amount of your income that is taxable, i.e., your tax withholding. It is advisable to revise it every year and make adjustments in congruence with life changes, for instance, marriage. Filing status is also quite important, and you may choose to continue filing your tax returns as an individual.

Claiming Deductions

Documenting expenses can often help you understand the deductibles you can claim, hence helping to lower your taxable income. If you have any of the documents below, compile them and submit them with your tax return to reduce your tax bill:

Charitable donations: records of all donations (itemized and non-itemized) to 501 (c)(3) registered charities. There is no upper limit on itemized cash donations; for those who claim the standard deduction, the maximum deduction is $300.

Homeownership documents: mortgage payments, property tax statements, moving expense records.

Medical expense records: hospital and doctors’ bills, health insurance payments, Medical Savings Account contributions. Try to itemize all expenditures greater than 7.5% of your adjusted gross income. For HSA’s, contributions up to $3,600 for individuals are tax-deductible.

Child Care expense documents: records of payments such as daycare or caretaker fees.

Educational expense documents: tuition fees payments, student loan payments, expenditure on courses/supplies that improve skills related to your job.

Retirement planning proofs: proofs of contributions made to IRA and 401k accounts. Contributions are up to $6,000 for those younger than 50 are tax-deductible.

State and local income tax payment records: this deduction is capped at $10,000 for any payments toward local and state taxes.

Claiming Credits

Tax credits can help reduce your tax liability as an individual filing tax returns. Using popular credits often results in a lower tax bill and larger refund. Keep the following documents handy:

Letter 6419: Child Tax Credits are worth up to $3,000 per qualifying child above the age of six and up to $3,600 for kids under six.

Form 1116: for claiming foreign income tax credits, i.e., income earned from assets in India.

Adoption documentation: for families with adopted children to claim Adoption Tax Credits.

Proof of financial support provided to a dependent: individuals taking care of dependents without a steady income claim Dependent Tax Credits. This credit significantly reduces liability to offset the costs incurred.

The Bottom Line

There’s nothing like the feeling of calm when confronting something as monstrously overwhelming as tax season. Being organized is the key to being prepared, so make sure to use this checklist to get your documents in order.

If you’re still unsure about the best way to file your returns and which deductions and credits are best suited to your situation, sign up for free with AOTAX today to get your questions answered.

AOTAX’s mission over the last 15+ years has been to help Indian IT professionals in the US. We have a dedicated team to solve all your queries and help you get the most from your tax returns.

With the golden ticket of H1B visa comes the clear path toward the American Dream. And of course, with the American Dream comes the American Reality—the brick-and-mortar behind-the-scenes that go towards building a life in the USA.

Tax returns are very much a part of this reality, and while reaping the system’s benefits may be smooth-wading through, the paperwork at the end of it is not.

However, filing your tax returns doesn’t have to be all drudgery and doom. Being organized is critical, and we help you out below with an extensive list of all the possible documents and forms you may need to file individual income tax returns.

Who Qualifies for Tax Returns in the US

However, before diving in, let’s quickly look at who exactly qualifies for paying taxes and receiving the returns that come with it.

To refresh, any individual who meets the ‘Green Card Test’ or the ‘Substantial Presence Test’ is considered a resident alien and thereby is liable to pay taxes in the same manner as any US citizen.

Here’s a breakdown of the two tests:

The Green Card Test—if you have not renounced your alien registration card (a green card), and neither has your privilege of immigrant status been terminated by the USCIS or a federal court, you pass the Green Card Test.

The Substantial Presence Test—you pass the SPT if you have been residing in the US for at least 31-days of the current year and 183-days total over the current year and the two years preceding it. More specifically, this count must include all days in the current year, one-third of the days present in the year before the current year, and one-sixth of the days present two years before the current year.

Now, let’s look at precisely what you need to file a complete and accurate tax return. To make things easy, we’ve grouped the documents according to their function.

Personal Information and Dependent Information

Basic information forms the crux of tax returns in the US, so it is essential to keep the following documents handy:

Previous tax returns and statements for reference.

Social Security or Tax ID numbers for both you and your dependents, if any.

Income-Related Documents

Furnishing proofs of earnings is an integral part of filing your taxes. As an Indian professional residing in the US, it is important to note that you are liable to declare your global income (from every source) in your tax returns.

That means earnings on mutual fund dividends, interest earned on stocks, bank deposits, and fixed deposits, among others, are all taxable. Below is a list of documents you may require while filing:

W-2 forms from employers.

Form 1040 to declare taxes paid in previous years and to declare foreign income.

Form 1099 series, each ending with a different suffix for different revenues earned. For instance:

1099-INT (interest income)

1099-G (government payments and tax refunds)

1099-K and 1099-MISC (freelance gig payments)

1099-R (pension income)

1099-S (stock sale income)

1099-B (property sale income)

1099-DIV (dividends)

1099-SSA (Social Security benefits)

Form 1095-A for Health Insurance Marketplace Statements.

Records of cryptocurrency transactions and interest earned.

Expense records such as bank or credit card statements.

Compiling the applicable documents below could help reduce the taxes you pay:

Records of donations to charity.

Homeownership documents such as mortgage payments and property tax statements.

Medical expense statements such as hospital and doctors bills and health insurance payments.

Childcare and educational expenses include daycare fee payments and tuition fees or loan payments.

Proofs of retirement account contributions.

Records of state and local income taxes paid.

Documentation for Credits

Tax credits are as valuable as deductions and help reduce your tax liability. It is important to have the necessary documentation in your tax return to claim these.

Here are some of the most common tax credits you can claim:

Child Tax Credits that are worth up to $3600 per child. Hold on to Letter 6419 for the same.

For foreign income tax credits, fill in and attach Form 1116 to your return to reduce the brunt of taxes paid on income earned back in India.

Adoption Tax Credits for families that have adopted children.

Dependent Tax Credits in case you are supporting a dependent while unemployed yourself. This credit reduces liability to offset the cost of paying for a dependent without a steady income.

Income Adjustments and Declarations

With personal and financial changes such as job changes, getting married, or having children, it is advisable to reconsider your withholding.

In a country with regulations far different from what we’re used to in India, preparing for tax season is taxing, saying the least. However, organizing your receipts, statements, and forms is an excellent first step to take.

However, filing on your own without knowing how to claim credits or deductions or whether you’re even eligible for them is doing a great disservice to your bank balance.

AOTAX has been helping Indian IT professionals in the US for more than 15-years and is well-versed in the challenges you face and how to get the best returns in your situation. Let us help you with our planning, advisory, and consulting services to ensure you only have to enjoy the American Dream while we take care of the American Reality. Sign up for free today to get a feel for how we work and what we can do for you.

It’s that time of the year when most Indians residing in the US are searching for whether and how to file tax returns online. The first question – do you even have to file taxes – is easy. The answer is yes, probably even if you are not a U.S. citizen.

If the government considers you a US tax resident (more on this later), then you have to report all income earned to the IRS and pay taxes. However, that does not automatically mean that your income will be taxable. You’re simply reporting it to the United States government.

The second question – how to file tax returns – is trickier. So, here’s a cheat sheet that tells you all you need to know about filing returns.

How to File Tax Returns Online for 2022?

The tax season begins on Monday, January 24, 2022. From that date, all permanent residents and tax residents can start filing their taxes. Also, even if you aren’t considered a tax resident, it is a smart idea to file them anyway. Why? You might qualify for a tax credit or be able to claim a refund.

Do green cardholders have to pay taxes?

Yes, all green card holders are US tax residents. They need to report all income and pay taxes, whether earned in the US or internationally. You must file tax returns using the IRS Form 1040 by April 15, 2022, even if you haven’t stayed in the US all year.

What about nonimmigrant visa holders?

If you’re in the US on a nonimmigrant visa, you may have to file taxes, depending on whether you’ve passed the Substantial Presence Test (SPT). The test declares that a nonimmigrant visa holder who has spent 31 or more days in the US in the current year is a tax resident.

You’re also a tax resident if you spend 183 days (calculated using a weight system) in “the current year and the two years immediately before that.”

As green card holders, all nonimmigrant visa holders use IRS Form 1040 to file taxes, and they have to do it by April 15th. The difference is that they only report income earned in the US. No taxes need to be paid for earnings outside the country.

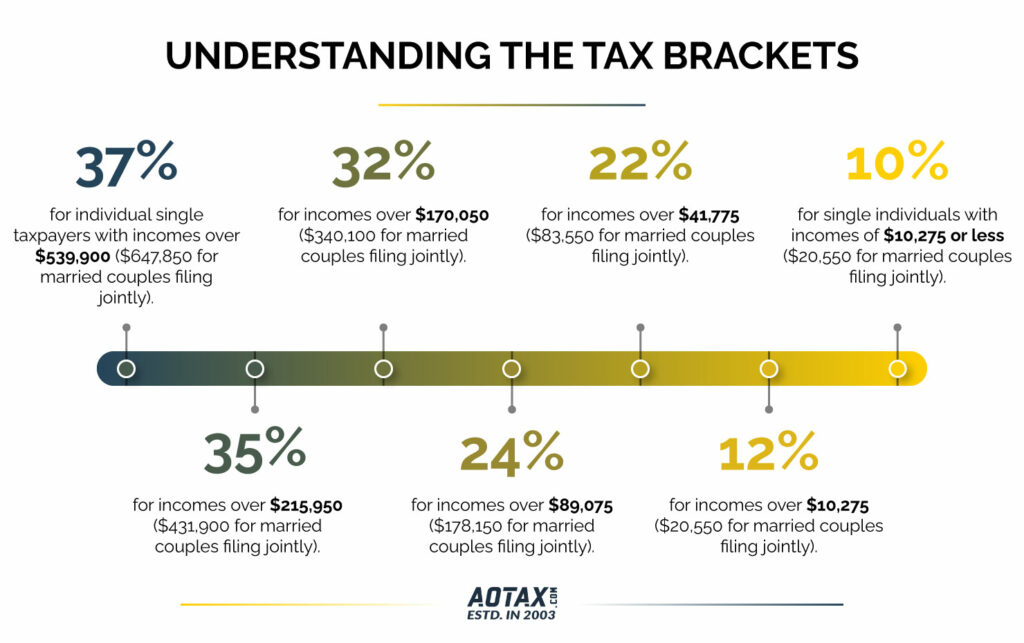

The US government uses a progressive tax system, so people with lower taxable income pay fewer taxes, and those with higher income pay more. So, how does the US calculate how much tax you need to pay? By dividing your income into tax brackets. Each bracket has its corresponding tax rate, and for this year, it is:

37% for individual single taxpayers with incomes over 539,900 ($647,850 for married couples filing jointly).

35%, for incomes over $215,950 ($431,900 for married couples filing jointly).

32% for incomes over $170,050 ($340,100 for married couples filing jointly).

24% for incomes over $89,075 ($178,150 for married couples filing jointly).

22% for incomes over $41,775 ($83,550 for married couples filing jointly).

12% for incomes over $10,275 ($20,550 for married couples filing jointly).

10% for single individuals with incomes of $10,275 or less ($20,550 for married couples filing jointly).

The benefit of a progressive system is that the tax rate does not apply to your entire income, irrespective of which bracket you fall into.

Pick how to file your tax return

You can file tax returns online, by hand, or hire a tax preparer. Filling out the Form 1040 manually and then emailing it is not a great idea because the process is much, much longer.

If you expect a refund, filing taxes online is better because the IRS processes e-filed returns faster. There is plenty of tax software that makes it very convenient.

The third option is to hire someone who provides tax preparation and filing services. You should strongly consider it if you are filing taxes for the first time, have never prepared tax returns using software, or have a complicated revenue stream. Professional guidance is crucial in the last instance.

Say you have a business that makes your finances complicated, or you also earn through a side gig, then a professional would make it easier to understand which forms are required, what common deductions to factor in, etc.

Collect all your documents

The last step before you sit down to file your tax returns online is to gather all your documents. You will need an ITIN, which is an individual taxpayer identification number. It’s issued by the IRS to people who do not have a Social Security number (SSN). You will also need to gather all:

Proof of income.

Proof of taxes already paid.

Proof of expenses to get tax credit or deductibles.

Filing taxes is never easy. But it becomes a daunting task the minute you get your provisional (and later permanent) green card. After that, you have to report all your income earned anywhere globally, even if you don’t spend a day in the US throughout the year.

For tax purposes, the US considers you their resident. It’s also a laborious task for Indians who have just gone to the US and filed their returns for the first time.

At AOTAX, we help Indians living in the US file their tax returns online. We’ve been doing this for a decade and a half with the help of an expert and qualified professionals. Besides tax preparation and filing services, we also offer tax planning advice, ITIN processing services, and extension filing. The entire process is online, making it effortless for you while ensuring you get the maximum returns possible! With AOTAX, you get to rest assured that your taxes are done right. Sign up and file tax returns online!

Tax Deductions Available for Cancer patientsA life-threatening disease like cancer can lead to a lot of mental unrest along with a lot of financial responsibilities. If you have a health insurance plan, then it would be helpful in providing cover for some amount of the medical expenses incurred. If you are undergoing any cancer related medical treatment then your health insurance would help in providing cover for the bills incurred. But, in the medical treatment related to these life-threatening diseases there would be some additional expenses which have to be paid by you. Also, cancer patients can avail the benefit of tax breaks on their taxes by the help of their out-of-pocket expenses.Eligibility for tax deductions which are cancer-relatedIf you are able to itemize your tax deductions instead of making claim for Standard Deduction, then you can easily deduct those medical expenses which are related to regular care, medication, diagnosis, hospital stays, etc. if the expenses that have been incurred are more than 7.5% of the Adjusted Gross Income (AGI).Medical-related travels can also be claimed as deduction such as the mileage related to driving to the appointment at the rate of 20 cents per mile as well as travel-related to any seminars. Those taxpayers who are self-employed do not need to itemize their tax deductions for deduction of their health insurance premium. Self-employed taxpayers are eligible to deduct their health insurance premium as a deduction to their income.What would be done?Medical expenses that can be deductible are defined according to the IRS code as those costs which are related to the diagnosis, treatment or mitigation of diseases and are mainly for the purpose of affecting any major body part or function. Various treatments related to cancer such as the chemotherapy and radiation surgery are too expensive and the arrangement of your health insurance plans will have a major impact on the coverage of these expenses.There are several categories of cancer and in case of any rare type of cancers such as mesothelioma which would need specialized care; travel is an important part of the treatment procedure. The cost involved in the travel during cancer treatment medical procedures might be tax-deductible.There is a comprehensive list of costs which would qualify for a tax deduction and this list would include health insurance premiums which are not paid in pre-tax dollars. You might pay for the medical care you have received by your credit card, cash or personal checks during the period of the tax year in which the tax deduction was being considered.During the time of tax return filing, itemized tax deductions such as the expenses related to medical bills, mortgage interest, State and Property taxes and charitable contributions will exceed the increased Standard Deduction that has been permissible by the IRS. The permissible Standard Deduction for the US citizens is $12,000 for those who are filing using Single status and is $24,000 for those citizens who are married and are filing their returns jointly.In case of your tax deductions being itemized, the medical costs incurred should be more than 7.5% of your Adjusted Gross Income (AGI) for the year 2019. Also, this figure was different for the tax year 2018 in which someone who has an AGI of $50,000 would deduct the expenses which are out-of-pocket if they are more than $3750.ConclusionHence, in case of any life-threatening diseases such as cancer tax deductions and claiming of credits is feasible but you must be well-aware about the tax rules and regulations.

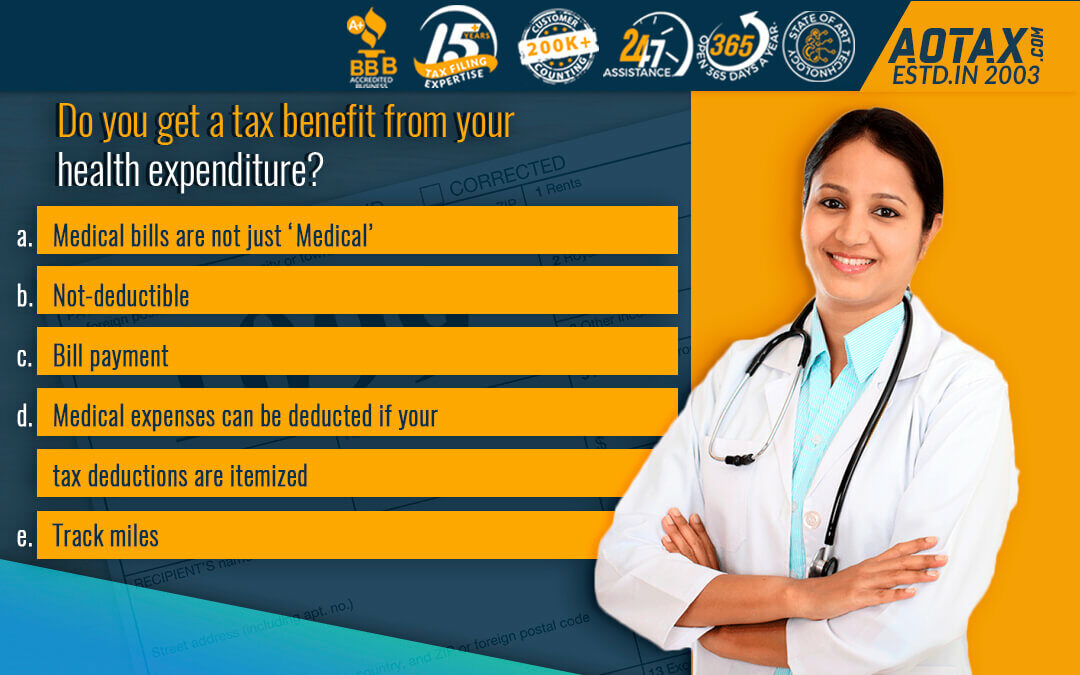

Do you get a tax benefit from your health expenditure?

It is very common to dislike paying medical bills even if you have very good insurance and a low deductible. One of the very bright sides of big medical bills is the chance you get to claim your medical expenditure as a deduction on the federal tax return. If your medical bills are more than 7.5% of your total tax years * the adjusted gross income (AGI) then it is quite feasible to itemize your deductions. The deductions on medical expenses are applicable for self, your spouse and for the medical expenditure of your dependents as well. In case, your medical bills are more than 7.5% of the income you obtain you must follow the below-mentioned rules for maximization of your tax refund.

Medical bills are not just ‘Medical’

The IRS would permit deductions on tax for vision and for dental care as well and also for the medical expenses too. This would imply that it is feasible to deduct the expenses incurred in the eye tests, dental-related visits, braces, contact lenses, glasses, root canal, etc.

Some other expenses which are covered under the category of medical expense deduction are psychological treatment, surgeries, medical devices such as hearing aids, medicines which have been prescribed, preventative care, etc.

Even the cost involved in your monthly payments of health insurance can be deducted if taxes have not been deducted by plans provided by the employer. The deduction for medical expenses would include the bills that have been incurred for yourself, your spouse and your dependents.

Not-deductible

You must have a complete idea about what is not tax-deductible before you have filed the tax returns. Any expenses which have been reimbursed either by the insurance provider or by your employer cannot be claimed as tax deductions. Moreover, if you are using a pre-payment plan for your medical expenses or are using a medical reimbursement plan then those expenses cannot be claimed as deductions. Some other non-deductible items would include your every-day supplies like toothpaste, soap, vitamins, etc.

Bill payment

Medical expenses can be deductible only if they are paid in the tax year in which you are filing the tax returns. Medical expenses can be claimed from the previous year or from any other future years. If a credit card has been used for the payment of medical bills in a tax year then it would be counted as being paid in a year and would be deductible as well.

Medical expenses can be deducted if your tax deductions are itemized

If you wish to receive the benefits obtained from the deductions obtained from medical expenses you must qualify for itemizing your deductions obtained on your taxes. Some of your itemized deductions such as property tax, State Income tax, home mortgage interest, etc. along with those medical expenses which are deductible need to be more than the Standard Deduction for the year 2020. In case you are self-employed, you would be able to deduct your premium for health insurance even if you are not able to itemize your deductions.

Track miles

You can track the medical mileage for the year 2020 and it is 17 cents for each mile. There can be travels related to the prescription pick up, emergency visits, appointments for the dentist and other medical check-up and follow up appointments.

Conclusion

Hence, if you have had medical expenditure during a particular tax year it would be completely worth it by maximizing your deductions and opting for itemized deductions. This would be helpful mainly when your itemized deductions are more than your standard deduction.

")

Recent Comments