Of course, being your boss comes with its own set of perks and perils: you can wear your pajamas to your home office or take a day off anytime you like. However, these advantages look bleak when you sit down to file your taxes, don’t they?

Moreover, tax filing as self-employed gets complicated if you are a self-employed non-resident Indian (NRI) in the US. So, we’ve put together a guide to help NRIs claim their tax breaks and reap the benefits.

What are the Tax Implications for Self-Employed NRIs in the US?

There are over 3.1 million NRIs in the United States, and most of them are self-employed. The Tax Cuts and Jobs Act (TCJA) of 2017 provides a 20% tax deduction on qualified business income (QBI).

NRIs and US residents can claim this deduction on their QBI. Thus, any income you earned while in the US is eligible for this deduction which expires in December 2025. In addition, there are 28 other deductions you can claim during tax filing as self-employed. Below we list out 14 such deductions:

14 Deductions and Benefits of Tax Filing as Self-Employed Individuals in the US

Freelancers and small business owners often worry about paying a significant chunk of their earnings to the IRS as taxes. However, they can avail of 28 other deductions and reduce their tax burden while filing as self-employed.

In addition, they can reinvest the saved money to grow their businesses.

Let’s take a look at some of these deductions:

1) Self-employment tax deduction

Self-employed individuals must pay 15.3% of their income as self-employment tax. The 12.4% goes to social security and 2.9% to Medicare.

This tax is paid by employees and employers jointly. However, you have to pay the entire amount as a self-employed individual. The good news is that you can deduct half of it from your taxes while filing as self-employed.

2) Home office deduction

If you work from home, you can claim a tax deduction for it. However, there are two formulas for calculating the amount: standard and simplified. For the standard option, you must keep track of all expenses such as electricity bills, repairs, and so on.

There is a pre-determined IRS rate for the simplified formula that changes each year. The current rate is $5 per square foot, and your home office should be no more than 300 square feet.

The best way is to calculate which formula provides the most benefit for you and apply it accordingly. For example, you can debit mortgage interest and depreciation if you own the home.

3) Deduction for internet and phone bills

Nowadays, almost all businesses are online and have a website. In this tax benefit, you can claim the costs of running the website, including internet connectivity.

Moreover, if you work from home and have a single phone line, you can deduct 100% of long-distance business phone calls. Nevertheless, if you have a second line for work only, you can claim back the entire phone bill from your taxes.

4) Health insurance premium

If your spouse’s healthcare plan does not cover you, deduct your healthcare premiums from your tax bills. However, if your plan covers your spouse, dependents, and children under the age of 27, you will gain extra benefits.

5) Meal deduction

The burger you ordered for work lunch is not tax-deductible. However, meals ordered during business travel or to entertain a client falls into this category.

The cost of entertainment, on the other hand, is not covered. Only food and beverages purchased from a restaurant qualify for this deduction. Currently, a full deduction is allowed, but it will expire after December 20, 2022.

6) Travel deduction

This deduction is available for business trips to meet new clients or learn new skills. While it covers the entire cost of transportation, only 50% of meals are covered. Moreover, the travel should be away from one’s work city and purely for business reasons.

7) Vehicle use deduction

If you are a baker, you can deduct the cost of driving your car to deliver your sweet treats. Instead, you can opt for the standard rate of 58.5 cents per mile.

Alternatively, you can opt for actual expenses that require you to record the times you drove your car for work. You can also claim tax incentives on vehicle repairs, insurance, and depreciation. Choose the formula which gives you the most benefit.

8) Interest deduction

The interest you pay on your business loan may be credited back to you through tax refunds. Nevertheless, you should use it for business purposes. For example, if you use the money for a quick trip to Hawaii, you will not receive tax benefits.

9) Education deduction

Being a student for life not only keeps you young but also generates tax benefits. As a result, taking courses to improve your current business skills will earn you a tax deduction. However, if you are a travel agent, a drawing course on Craftsy is not tax refundable.

10) Deduction for business insurance

Insurance is taken to protect your business, office space, and equipment, such as fire insurance, car insurance, and credit insurance, which is also tax-deductible.

11) Rent deduction

Renting office space, office equipment, or canceling a business lease is tax-deductible. However, you cannot deduct the rent if you own the space.

12) Deduction for startup costs

Startups can claim a maximum of $5000 for a business. In addition, startups can deduct their market research costs, travel expenses, attorney and accountant fees, and advertising costs in this segment. If their startup is an LLC or corporation, they can deduct an additional $5000 in organizational costs.

13) Advertisement deduction

Money spent on Facebook and Google ads, as well as on billboards, are tax-deductible.

14) Deduction for retirement plan contributions

This deduction is an investment in your future security. When you purchase a Simplified Employee Pension plan, the premium is tax-deductible.

These and other deductions are detailed in Schedule C of Form 1040, downloadable from the IRS website. Take advantage of it now and reap the rewards later. First, however, keep all records, receipts, and documents for the mentioned expenses if you are filing as self-employed. If the IRS conducts an audit, these will be used to support your claims.If you are a self-employed NRI in the United States and are unsure how to file your taxes, contact AOTAX. With over 15 years of experience in US taxation laws, we have helped over 2 million tax compliant. Our tax experts will assist you in tax filing as self-employed.

Small businesses have enjoyed consistent growth in the US in the last few years. There were 32.5 million such enterprises in 2021, up 2.5% over 2020. And a 9.8% increase in the previous four years.

These small enterprises are job providers for freelancers and independent contractors. According to statistics, approximately 70% of such businesses hire freelancers.

The IRS (Internal Revenue Services) requires these entrepreneurs and freelancers to fill out the 1099 form. And refusing to comply with this has repercussions. So, if you are an Indian freelancer or a small business owner in the US, we will tell you how to fill out a 1099 form.

What is a 1099 Form?

A 1099 form is used to report a freelancer or independent contractor’s non-employment income of $600 or more. It includes revenue from stock dividends, interest on deposits, property sales, cash prizes, royalties, and other sources.

The IRS receives this form straight from the payer. Therefore, the taxpayer doesn’t need to file it in their income tax return (ITR). They are, nevertheless, required to inform the IRS about these transactions.

Who is included under the 1099 category?

With nearly 59 million freelancers, the USA is regarded as the largest freelancer market in the world. And out of this figure, 36 million do it on a full-time basis.

Every year freelancers contribute $1trillion to the US economy. As a result, their earnings must be reported on the 1099 form. In addition, businesses that hire their services must also file the 1099 form with the IRS.

They do not need to fill out this form if they hired freelancers or contract workers through a third party like Fiverr, Upwork, or Freelancer.com.

Types of 1099 form

A non-salary income has varied forms – like consulting fees, dividends, interest, retirement payouts, tax refunds, and so on. And the 1099 form has a different category for each of these. We will show you how to fill out the 1099 form for payments made or received:

1) 1099 NEC – A company that paid $600 or more to an independent contractor or freelancer for work in the last fiscal year must fill out this form. Similarly, if they paid $600 or more to an attorney, they are subject to 1099 NEC.

2) 1099-DIV – If a person receives dividend income from their stocks, they will receive a 1099 DIV. The company will send them this form.

3) 1099 – INT – Individuals who earned $10 or more in interest in the preceding year will receive this form from banks and brokerage firms.

4) 1099 G – People who receive federal, state, or local government tax returns or unemployment benefits also receive 1099-G.

5) 1099-R – This form is also issued to those receiving money through a retirement or pension plan or individual retirement account (IRA). In addition, certain annuities and insurance contracts also fall in this category, though they may or may not be taxable.

6) 1099-S – This form is used to report the sale of land, which might be residential, commercial, or industrial.

7) 1099 MISC – This category includes money received as cash, reward, award, royalties that were not earned through employment.

How to Fill Out a 1099 Form?

The 1099 form has two copies – A & B. When a business owner hires a freelancer, they must fill in copy A and send it to the IRS. And send copy B to the freelancer. Both the copies should be sent to the IRS before January 31.

Employers can submit physically or electronically. If they do it physically, they must also submit the 1096 form. They have to do it on the IRS Filing a Return Electronically (FIRE) system for online submission.

Moreover, unless the freelancer is a non-resident or resident alien, the form should include the following information – legal name, residence, the total amount paid in the previous year, and social security number.

The contractor should also consent the business owner to receive 1099 by email or paper copy.

Deadline

The IRS requires the taxpayers to report their 1099 income by January 31 of each year. The businesses must file by the end of February. Whether a taxpayer has received their 1099 or not, they must report such income to the IRS.

Notify about your changed address

If you are a freelancer and have changed your address, ensure that you receive everything the IRS sends. Hence, inform your payers (employer) about the address change.

Correction of errors

If freelancers receive 1099 from their payers with any errors or discrepancies, they should contact the latter to correct it before January 31. If the payer fails to rectify the errors, the freelancer should inform the IRS about it in the tax return form.

Penalties

If a freelancer/independent contractor fails to file/report their 1099 on time, they will be subject to the following penalties:

1) A delay of 30 days after the due date costs $50.

2) A delay of 30 days or more till August 1 costs $100.

3) If submitted on or after August 1, the fees will be $260.

4) If you fail to file it, you must pay a minimum of $530.

Being a law-abiding US citizen and the taxpayer is good for you. And if you follow the above instructions, you can easily fill out or report your 1099 forms. It will also keep you out of trouble with the IRS.

If you have trouble filling your taxes, contact AOTAX to help you do so. With us, filing your tax returns will be a breeze, thanks to their staff of expert tax planners and skilled advisors. For any more information, visit us on Home – AOTAX.

Is a complete understanding of the US taxation system still eluding you?

Does the complexity and endlessness of IRS forms overwhelm you?

Well, we’re here to tell you that you are not alone.

Thousands of Indian IT professionals embark to America for better pay and jobs and often get caught up in the confusing web of filing their tax returns.

A new country and different laws can complicate tax season, but you can better handle it with some preparation and organization. So we’ve come up with the ultimate checklist to help you prepare for filing your taxes.

What are the Documents Required for Income Tax Return of Individuals?

Depending on your financial and personal context, the claims you make while filing your tax returns can vary. Therefore, multiple documents are often required, which can be hard to track.

Nevertheless, we’ve categorized the documents required for income tax return of individual per the functions they serve while filing your taxes. Read on to know exactly what you need to keep handy to sail through the tax season smoothly:

Personal Information and Dependent Information

Basic identification information is mandatory while filing tax returns. Be sure to include the following documents:

Previous tax returns and statements for reference. The IRS has up to three years to decide on whether to audit an individual or not. In such a scenario, having copies of previous tax returns is necessary to ensure the best outcome.

Social Security or Tax ID numbers and dates of birth of both you and your dependents, if any. Dependents include spouses, children, parents whom you provide for financially. In the case of child dependents, furnishing childcare records is advisable.

Income-Related Documentation

Your total income determines your tax bracket and how much tax you pay. However, you are legally required to file taxes for all the types of income you receive, including rental income, interest on investments, and profits made on anything you choose to sell in the year.

In addition, the US Government taxes Indian H1B holders on their global income and their US income. Therefore, you must declare any profit-generating assets back in India as a part of your income. It is advisable to keep the documents below ready and submit them as a part of your tax return:

Form W-2: issued by your employer and states precisely how much tax was withheld from your pay.

Form 1099 series: each form in this series has a different suffix to indicate the different types of revenues possible:

1099-INT: for income in the form of interest earned on investments.

1099-G: for government payments and tax refunds.

1099-K and 1099-MISC: for payments received for freelance gigs.

1099-R: for pension income.

1099-S: for income received upon the sale of stocks.

1099-B: for income received after selling a property.

1099-DIV: for dividends received for mutual fund investments.

1099-SSA: for Social Security benefits.

Form 1040: to be used while declaring foreign income and reporting taxes paid in previous years.

Cryptocurrency transaction records of sales, if any, and interest earned.

Form 1095-A: for Health Insurance Marketplace Statements.

Rental asset records: for income earned in the form of rent.

Expense records: bank and credit card statements.

Form W-4: for changing the amount of your income that is taxable, i.e., your tax withholding. It is advisable to revise it every year and make adjustments in congruence with life changes, for instance, marriage. Filing status is also quite important, and you may choose to continue filing your tax returns as an individual.

Claiming Deductions

Documenting expenses can often help you understand the deductibles you can claim, hence helping to lower your taxable income. If you have any of the documents below, compile them and submit them with your tax return to reduce your tax bill:

Charitable donations: records of all donations (itemized and non-itemized) to 501 (c)(3) registered charities. There is no upper limit on itemized cash donations; for those who claim the standard deduction, the maximum deduction is $300.

Homeownership documents: mortgage payments, property tax statements, moving expense records.

Medical expense records: hospital and doctors’ bills, health insurance payments, Medical Savings Account contributions. Try to itemize all expenditures greater than 7.5% of your adjusted gross income. For HSA’s, contributions up to $3,600 for individuals are tax-deductible.

Child Care expense documents: records of payments such as daycare or caretaker fees.

Educational expense documents: tuition fees payments, student loan payments, expenditure on courses/supplies that improve skills related to your job.

Retirement planning proofs: proofs of contributions made to IRA and 401k accounts. Contributions are up to $6,000 for those younger than 50 are tax-deductible.

State and local income tax payment records: this deduction is capped at $10,000 for any payments toward local and state taxes.

Claiming Credits

Tax credits can help reduce your tax liability as an individual filing tax returns. Using popular credits often results in a lower tax bill and larger refund. Keep the following documents handy:

Letter 6419: Child Tax Credits are worth up to $3,000 per qualifying child above the age of six and up to $3,600 for kids under six.

Form 1116: for claiming foreign income tax credits, i.e., income earned from assets in India.

Adoption documentation: for families with adopted children to claim Adoption Tax Credits.

Proof of financial support provided to a dependent: individuals taking care of dependents without a steady income claim Dependent Tax Credits. This credit significantly reduces liability to offset the costs incurred.

The Bottom Line

There’s nothing like the feeling of calm when confronting something as monstrously overwhelming as tax season. Being organized is the key to being prepared, so make sure to use this checklist to get your documents in order.

If you’re still unsure about the best way to file your returns and which deductions and credits are best suited to your situation, sign up for free with AOTAX today to get your questions answered.

AOTAX’s mission over the last 15+ years has been to help Indian IT professionals in the US. We have a dedicated team to solve all your queries and help you get the most from your tax returns.

Taxpayers should file IRS Form 8962 with their federal income tax return to claim the Premium Tax Credit (PTC). The PTC is intended to assist taxpayers in recouping some of the costs of health insurance purchased through the health insurance marketplace.

Taxpayers reconcile the tax credit they are entitled to with any advance credit payments for the tax year using Form 8962. In addition, to qualify for the PTC, taxpayers or their family members should have been enrolled in a health insurance program through the marketplace for a minimum of one month during the tax year.

The cost of available health insurance, the size of the taxpayer’s family, where the taxpayer lives, and the address determine the tax credit amount. Hence, if you receive healthcare from your employer (1095-C form), you will not file Form 8962. Also, if you have health insurance through another company and have received a 1095-B form confirming your coverage, you cannot use Form 8962.

Given all the terms and conditions regarding the Form, it could get challenging to fill the same. If you’re wondering how to fill out Form 8962, then you’re on the right page.

What Is Advance Premium Tax Credit

The advanced premium tax credit is a federal tax credit for individuals that reduces the monthly health insurance premiums they must pay when purchasing coverage through the Marketplace.

When you sign up for a qualified health plan on the health insurance marketplace, the system determines whether you are eligible for a subsidy. The marketplace determines your eligibility for a subsidy based on your income and personal exemptions, known as an advance payment or APTC.

You should report any changes in your income or personal exemptions to the marketplace if they occur throughout the year. If you do not, you might receive too much or too little in APTC.

On the other hand, if your income increases and you do not declare it, the government may pay you or your insurer too much APTC. In such a case, you use Form 8962 to reconcile your PTC eligibility with the APTC already paid.

If you are qualified for more PTC than you were paid in APTC, you may be able to get the difference you paid back in your tax return.

For 2021 and 2022, the American Rescue Plan Act of 2021 eliminates the advanced premium tax credit income cap. Instead, on the high end, the act caps premiums at 8.5% of the payer’s modified adjusted gross income (i.e., for people with adjusted gross income above 400% of the poverty level).

The “net Premium Tax Credits” are also claimed using Form 8962. These are for qualified persons who, instead of receiving an APTC, choose to pay their insurance premiums out of pocket throughout the year and then claim the PTC at the end of the year.

Points to Consider Before Filling Out Form 8962

These are some things you should consider before starting the filing procedure. This checklist will help you keep track of the validity and authenticity of your filing process:

Either you or a member of your family must be enrolled in a health plan covered by the “Market Plan”.

As a recipient, you are lawfully residing in the US. This is to establish residency.

To complete the filing of Form 8962, an extra Form 1095-A is necessary.

The marketplace sends this, and if you haven’t received it by early February, you have to contact them.

The PTC estimate provided by the Marketplace is likely to decide your Advance PTC eligibility.

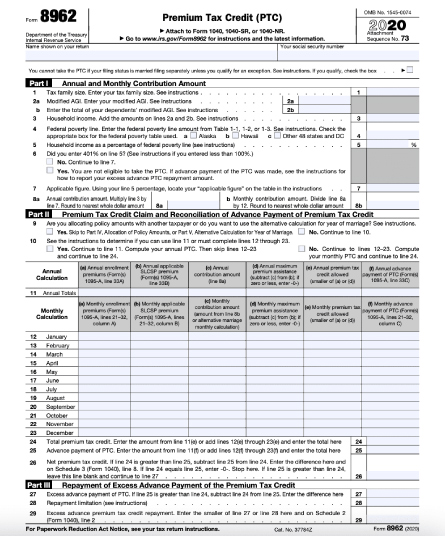

Reading Form 8962

Form 8962 is a two-page document with five sections:

Part I is where you enter the annual and monthly payment amounts based on the size of your family, modified adjusted gross income, and household income.

Part II is where you balance the amount of your advanced premium tax credit with the amount of your monthly premiums.

Based on the information you supplied in Part II, Part III is utilized to determine any excess advance premium tax credit payments.

Part IV permits you to assign policy funds, whereas Part V is utilized for alternative calculation of your year of marriage.

To complete each component of the form, you’ll need Form 1095-A, as well as your Form 1040, which shows your modified adjusted gross income.

If the information on your Form 1095-A is incorrect, you must update it before filling out Form 8962. Contact the Health Insurance Marketplace to receive an updated form.

Download the Premium Tax Credit (Form 8962)

The IRS website has Form 8962, which is free to download. When you move through the program’s questionnaire format, this form should be generated for you if you’re filing taxes electronically.

Instructions for IRS Form 8962: A Complete Guide

If you’re unsure how to fill out Form 8962, follow the steps below to learn everything you need to know:

Step 1

First, you’ll need to obtain IRS Form 8962. You can get it from:

The Treasury Department

IRS website

Step 2

You will receive a PDF file of the form. Now, you will begin the filing procedure.

Fill in your name as it appears on your tax return and your Social Security number at the top of the form.

Step 3

Next, go to “Part 1” of the form. Begin by filling in the exemptions from Form 1040-A on the first line. Next, you should enter the amounts relating to the updated AGI on lines 2A and 2B. Next, you must add the Household Income to line 3; to do so, simply add the numbers from lines 2A and 2B. To complete line 4, simply select the appropriate option and enter the proper value. Finally, add the household income in terms of the percentage of the Poverty Line on line 5. Skip to line 7 if your value is more significant than 401%.

Step 4

In Line 7, enter the needed figure, and then in Line 8, enter the annual contribution amount.

Step 5

Now, we’ll go to Part 2 of IRS Form 8962. The name of this section is: “Premium Tax Credit Claim and Reconciliation of Advance Payment of Premium Tax Credit.” Proceed to Line 11 after selecting the proper options on Lines 9 and 10. There’s a little table to fill up the monthly amounts column-by-column. You’ll fill up the lines 12-23 due to this. Line 24 (Total PTC) is below the table and is where you must add the Total PTC. Then comes Line 25, where you must enter the Advance payment.

Step 6

We shall not continue to Part 3 of the application. This section is known as “Repayment of Excess Advance Payment of the Premium Tax Credit.” So instead, we’ll go on to Line 27, where you’ll need to fill in the ‘Advance Premium Tax Credit.’

Step 7

This section is known as “Shared Policy Allocation.” Lines 30-33 make up this section. You must fill in the values in the table that is provided, which includes:

The policy number is entered in the field a.

SSN field (field b).

In Field c, enter the allotment for the first month.

Fill in the allotment ending the month in Field d.

The premium % should be entered in field e.

In field f, enter the SLCSP percentage.

In field g, enter the advance payment for the PTC percentage.

Step 8

This section is the “Alternative Calculation for the Year of Marriage”. Add the alternate entries for your Social Security Number in fields a, b, c, and d when you get to line 35. Then, add the alternate entries for your spouse’s SSN on fields a, b, c, and d when you get to line 36.

Final Thoughts

Whether you receive an Advance PTC or claim a PTC at year’s end, you must file Form 8962 with your tax return if you purchase health insurance through the Marketplace and qualify for Premium Tax Credits (PTC). In addition, your local health exchange should send you a Health Insurance Marketplace Statement (Form 1095-A) to assist you in filling it out.

Are you wondering how to fill out Form 8962?AOTAX makes preparing and filing your taxes quick, easy, and affordable so that you get your maximum refund.

We are Registered Tax Agents with vast hands-on expertise, and we take great pride in assisting our clients in achieving their objectives. Thanks to a team of highly skilled and experienced Tax Accountants, we do everything we can to reduce your tax liability while making the overall taxation process as efficient, simple, and cost-effective as possible. Contact us if you are an IT professional working in the USA and looking at filing tax in the USA.

Are tax filing woes quickly becoming the bane of your existence? Have you let the financial year pass by without considering your potential tax burden and how to alleviate it? Unfortunately, many individuals fall prey to last-minute scrambling when it’s often too late to make any changes.

As H1B visa holders, Indian professionals are taxed the same way as US citizens and can claim certain deductions and credits. However, lowering your tax bill is not as simple as it seems.

Efficiently managing your finances requires the implementation of tax planning strategies. These strategies, if well-timed and well-executed, help individuals avoid tax penalties.

The road to filing taxes is long and necessitates constant vigilance and planning all year long. We take you through some essential tax planning strategies for individuals to implement them to make tax season easier.

You can effectively forecast and plan financially toknow which tax bracket you fall into. It is essential to understand that the United States has a progressive tax system—taxable incomes are usually not the same as your total income.

The difference is determined by, and due to, your filing status and the deductions you claim. Hence, the strategies you implement will also be determined by your taxable income figure.

2. Documentation: know what to keep and what to throw

Undoubtedly, the most critical component of tax filing is organized documentation. Having a record of expenditures and statements for the current financial year is as essential as having copies of previous tax returns that date back at least three years.

Why? The possibility of audits. The IRS has three years to decide whether to audit an individual or not. For Indian H1B holders who are taxed on their global income (income earned from investments back home), tax filing should be treated with extra caution, and documentation must leave no room for ambiguity.

3. Tax savers: deductions and credits

Tax deductions and credits are powerful tools and can significantly reduce tax burdens when used correctly. Deductions lower your taxable income, while credits reduce the tax value itself, giving you a larger refund. Below are some of the most popular ways to use these tools to get a more significant tax break:

Retirement planning

Growing your nest egg for retirement while reducing tax bills may sound too good to be accurate; but individuals can maximize savings by making contributions to retirement funds.

Whether you choose to participate in 401k or IRA plans, all contributions up to $6,000 for those younger than 50 lower your taxable income.

Kiddie taxes and child tax credits

For individuals with kids, children’s unearned income (investment-type income) above $2,200 must be taxed using their tax rates, and parents are advised to take note of the same.

Additionally, parents could claim child tax credits on their taxes, which means receiving up to $3,000 per qualifying child above the age of six and up to $3,600 for kids under six.

Educational expenses

Tuition fees, supplies, and other expenses made on classes or courses that improve skills related to your job may be deducted from your taxable income, thereby saving you money.

Health insurance and medical expenses

Medical bills can be financial drainers. So while filing for 2021, make sure to itemize all expenditures that are greater than 7.5% of your adjusted gross income, as they can be tax-deductible.

State income and local tax deductions

Individuals can deduct amounts paid either toward state income taxes or local and sales taxes from their taxable income. The deduction is capped at $10,000 and provides a sizable tax break.

‘Other dependent’ credits

Aside from claiming credits for dependent children, individuals also have the option of claiming credits up to $500 for anyone they may be supporting financially.

Flexible spending accounts & health savings accounts

FSAs and HSAs are valid accounts to have, especially when taking care of your health. So catch up on doctor’s visits, and don’t let your FSA balance go to waste.

As for HSA’s, contributions up to $3,600 for individuals are tax-deductible.

4. Reevaluate filing status and change tax withholding allowances

The IRS recommends yearly tax withholding allowance adjustments to ensure the taxes withheld from your paycheck are best suited to your current needs.

Revisiting your W-4 to check filing status and tax deductions might be a good idea if you’ve experienced any of the following the past financial year:

Getting married

Having children

Unemployment

Salary increments or reductions

Changing jobs

5. Harvest losses

This year, it may be profitable for individuals who jumped on the investment bandwagon to minimize capital gains. You can do so by offsetting gains with losses worth up to $3,000, thereby reducing your taxable income.

6. Donate to charity

Charitable giving is a noble action, and individuals are further incentivized to continue since donations are tax-deductible. Any donations made to a 501(c)(3) registered charity are deductible.

For 2021, there are no limits placed on the number of cash contributions made for those that itemize their deductions. For individuals who claim a standard deduction, the deductible is $300.

7. Work with a professional

Organizing and optimizing your tax returns is no easy task, especially when there are so many things to consider being an H1B holder.

However, handing over the reins and collaborating with seasoned tax planners and professionals can make all the difference to how much money is put back in your pocket.

Having the right people analyze your finances helps you make more intelligent and strategic decisions all year round, and we at AOTAX do precisely that.

Our team has been in the business of assisting Indian IT professionals for close to twenty years. You can trust us to help you get the best returns. So sign up for free today!

Recent Comments