Bookkeeping entails more than just keeping track of your company’s finances. It enables you to understand where you stand as an entrepreneur and to plan for your company’s future growth. It also informs investors about your company’s financial health, attracting more investment. It even aids you in tax audits and protects you from the IRS.

If you are an Indian who owns a business in the US, having a good bookkeeping service is a great idea. We reveal the secrets that will transform the way you think about bookkeeping. If you are still debating hiring bookkeeping services near you, then read on to know why you should go for it.

What Exactly is Bookkeeping?

Bookkeeping is a part of financial management that aids in the development of a company’s growth strategy. Simply described, it is an accounting tool used to keep track of a company’s financial records. These books record every dollar related to your firm, including cash flow, costs, salaries, sales tax, and so on. It’s a must-have survival tool for any company looking to expand.

Components of Bookkeeping

Bookkeeping is more than keeping a record of your business income and expenditure. It also takes care of your cash record, inventory, assets record, profit and loss accounts, payroll, sale invoice, revenue, and other financial transactions. This data is in the form of a financial statement.

9 Reasons that will Alter your Perception of Bookkeeping Services

If you’ve just launched a small business and think you can get away with skipping bookkeeping for a few months, you’re in for a rude shock. The longer you wait to hire a bookkeeper, the more confusion you’ll create for yourself and your business. You’ll need a professional bookkeeper to maintain proper books of accounts to function smoothly. They will not only keep track of your cash register but will also update you about your company’s financial health. In addition, a qualified bookkeeper will assist you with financial statements, IRS audits, and tax benefits, among other things. Here are a few ways in which bookkeeping helps businesses succeed that will get you looking for bookkeeping services near you right away.

1) Budget

A sound budget is a foundation for a successful business. Bookkeeping helps you manage your budget by monitoring the income and expenses. You may be left clueless about your cash reserves if you don’t keep adequate records, risking the chance of outrun or higher cash burn rate. Bookkeeping allows you to calculate your earnings and expenses, assets and liabilities, and plan for future business growth.

2) Tax-Compliance

Having a good bookkeeping system in place makes it easier to stay on top of your taxes. During tax season, one does not have to look for receipts or papers because all the financial data is already documented. Hiring a bookkeeper near you to keep the IRS away saves you a lot of time. And in case the IRS comes knocking, the bookkeeper can also assist with the financial audit.

3) Organization

Bookkeeping aids you in being organized and systematic in your business. Every dime that comes in and goes out of your company is tracked and documented. As a result, you may confront any IRS audit with confidence because all financial data is easily available. Furthermore, you can quickly offer your investors and lenders the data to obtain more loans and credits.

4) Analysis

Bookkeeping assists you in conducting a thorough analysis of your business. The cash influx and outflow and its impact on business growth are detailed in the financial statements that are generated regularly. By examining the data, you can determine which company strategies are profitable and which should be abandoned. It allows you to make specific tweaks that will help your company flourish.

5) Planning

Your business’s well-documented financial records assist you in planning for future expansion. Bookkeeping also aids in tax planning by allowing you to take advantage of specific tax incentives. For example, you can claim meal deductions for business luncheons on your ITR.

6) Bill and Other Payments

Keeping track of your bills, loans, taxes, and rent payments are excellent bookkeeping practices. You save time and money by settling these on time instead of paying penalties or late fees.

7) Goal-Setting

Bookkeeping can assist you in achieving professional objectives. It allows you to develop financial plans and forecasts for your company’s growth by presenting financial data at your fingertips.

8) Cash Flow Management

It not only allows you to manage but also boosts your cash flow. Bookkeeping assists you in keeping track of consumer and vendor invoices. You can request early payment from your consumers and pay the vendor on or near the due date. This would free up additional cash for you to invest in your company.

9) Peace of Mind

If you practice effective bookkeeping, your financial records will be well-organized. You don’t have to be concerned about dealing with banks, investors, or the Internal Revenue Service. You are at ease and can concentrate on growing your business.

Thus, having a bookkeeper serves you at multiple levels. It keeps you organized, safe from the IRS, helps you move towards your goals, and lets you control your finances. It takes care of your financial worries so that you can focus your energy on business expansion. In a nutshell, a bookkeeper and accountant are what you need to make your business a success.

If you are an Indian business owner working in the United States looking for bookkeeping services near you, contact AOTAX today. Our team of skilled bookkeepers will help you get your financial books on track. We have over 15 years of experience in the relevant field and have helped over 2 lac Indian professionals and businesses get their books and taxes in order.

Do you need to travel outside the US this April? Are you short on time to file your federal tax returns? Then it would be a good idea to file a personal tax extension with the IRS. If you are an Indian in the US who is unsure to file a personal tax extension, we can help you.

Our easy 8-step guide will walk you through the process on how to file a tax extension in eight easy steps.

But, first things first.

What Is Personal Tax Extension Form 4868?

The deadline to file federal taxes in the United States is April 15. However, many people are unable to meet the deadline due to various reasons. In this scenario, one can fill out Form 4868 to file a personal tax extension. However, you have to submit this form to the IRS (Internal Revenue Services) before the due date. This will let you avail a six months extension till October 17 to file your income tax returns (ITR).

However, this extension is on filing the ITR and not on the tax payment. You will be required to make the income tax payment by April 15. Failing to do so will attract penalties. Moreover, this form is to be filled by individuals and not by businesses or corporations.

Form 4868 is available on the IRS website. You will need the following details to complete the form:

Your social security number (and your spouse’s too if filing a joint return)

Address

Estimate of tax liability for the year

Taxes already paid (tax withheld by an employer)

Calculation of deductions and credits

Where to file?

Filing a personal tax extension is easy, free, and convenient. One can file it electronically on the IRS website. Or print a form from the website, fill in the requisite details and mail it to the IRS directly.

How To File A Personal Tax Extension?

Filing a personal tax extension may sound more difficult than it is. But it is convenient if done before the due date. Here is a guide to help you file a personal tax extension:

1. Electronically

You can use IRS Free-file (IRS Free File | Internal Revenue Service)to file a personal tax extension via form 4868. Once you fill in the required information and make the tax payment, you will receive an acknowledgment from the IRS. Keep it as a record to submit it in October when you file your returns. One can use Free File to file form 4868 if their adjusted gross income is under $73,000 for the last financial year. If your income is above the threshold, opt for the IRS Fillable Forms tool(Free File Fillable Forms | Internal Revenue Service (irs.gov) to file for a personal extension. Your tax preparer can also help you with it.

2. Mailing A Tax Extension Request

If you are planning to send your request for a personal tax extension by mail, print form 4868 from the IRS website. You can also get the form from your local post office or the IRS.

Fill in the details, attach your tax payment check, and mail it to the IRS. Snail mail takes time, so rather than waiting until April, do it now.

3. Tax Payment

Form 4868 buys you more time to file your taxes. However, this does not defer your payment till October. One is required to pay their dues by April 15. Hence, you can pay a portion or all of your taxes online through a debit or credit card, or DirectPay. You can also mail a check or send a money order to the ‘United States Treasury’ along with your form 4868.

4. Special Tax Payment Extensions

Certain individuals get an automatic 60 days extension on filing and payment of their ITR. These are citizens or resident aliens of the United States who live outside of the United States or Puerto Rico. They could be serving in the military or on the naval outside of the United States or Puerto Rico.

Similarly, those in the Armed forces working in combat zones in or outside the US also get 180 days tax payment extension. All the above-mentioned individuals should explain the reason for the delay when they file their returns. However, if you owe taxes to the IRS by the due date, be prepared to pay the interest on the amount accrued.

5. Tax Extension Approval

If you apply for a tax extension online, you will receive confirmation within 24 hours. However, you may need to phone the IRS office to see if your request has been received if you’ve sent it via snail mail. The IRS will usually allow you an extension unless there is a problem with your form. And will not contact you unless there is a problem with your form.Also, you will not be contacted by the IRS if you have filled the form properly.

6. Tax Payment Options

If you can’t pay your taxes in full by the April deadline, you can choose to pay them in installments. The IRS’s website allows you to select a payment plan.

7. Tax Relief Options

If you require tax relief due to financial difficulty, you must file Form 843 (Form 843 (Rev. August 2011) (irs.gov). The same holds if you haven’t paid your taxes in a while or if the IRS has given you incorrect written advice. You can file an appeal if they reject your request.

8. State Tax Extensions

The above method is applicable for federal tax extensions. Some states offer a six-month automatic personal tax extension, while others do not collect state taxes at all. For more information, get in touch with the appropriate state officials.

It is easier to file a personal tax extension if the preceding steps are followed. Do not, however, use it as an excuse to pay your taxes late. You’ll get in trouble with the IRS and face a penalty if you do.

Are you still skeptical about filing a personal tax extension yourself? Then we are here to help you out. Use the services of AOTAX to remain on top of your tax deadlines. Over 2 lac Indians have benefited from our team of skilled tax consultants and planners who have helped them submit their US taxes on time.

As a relatively new resident in the US, there are many things to adjust to – a different culture, new sights, distinct workplace norms, and unfamiliar financial regulations. With so many things to get used to as an Indian professional in the States, taxes definitely sit high on the priority list.

IRS guidelines and the tax return system can be confusing, especially to newcomers who are unaware of the finer details that need to be considered when filing their income tax returns. The implications can include large and unnecessary financial losses. The best way to avoid receiving lower refunds and incurring penalties is to file your tax returns correctly.

What Are Some Common Mistakes That Individuals Make?

Mistakes are meant for learning, not repeating. That’s why we’ve compiled a list of the most common errors individuals make in their tax filings. Read on to know more about what they are, and how you can avoid them, while simultaneously maximizing returns.

1. Not Being Aware of Important Deadlines

Having a clear idea of important dates on the tax calendar can help you plan financially according to payment deadlines and refund dates, which is something many people neglect to consider. Paying your taxes on time and budgeting expenses according to when you’re likely to receive your refund can greatly ease financial burdens. Additionally, respecting IRS deadlines means you can avoid any nasty penalty fees, and also make the most of deductible contributions within the requisite timeframes. Being a fiscally responsible resident can help you avoid unnecessary legal obstacles, and does wonders for your personal finances.

2. Not Proofreading Your Forms

As is rightly said, the devil is in the detail. A shockingly large number of US residents receive delayed refunds because of their own doing. Silly spelling mistakes and small discrepancies in values declared on tax return forms can cause delays that can last weeks or even months.

Even the smallest of errors could result in you having to redo your taxes altogether, so make sure the information matches what is given on forms such as the W-2, or 1099, etc. Always remember to dot your I’s and cross your T’s!

3. Not Checking Your Eligibility and Residential Status

As an Indian professional and H1B visa holder, the Substantial Presence Test is an important component of being able to reside in the country legally and to receive the requisite benefits from paying taxes. The SPT is used to determine how long you have been in the country, and whether you are considered a resident for tax purposes. For more information, visit the IRS webpage.

4. Not Safeguarding Important Documents

Documentation is undoubtedly the most significant facet of filing your tax returns. The taxes you are liable to pay, and the refund you are eligible to receive, both hinge on the supporting documents you provide. This includes financial statements, mortgage statements, letters from the IRS substantiating credits you have claimed, etc. Additionally, keeping past tax returns is equally critical in protecting against potential audits. The IRS has up to three years to decide whether to audit an individual and in the event you are audited, the records can make the process easier.

5. Not Checking Tax Brackets or Adjusting Tax Withholdings

Life is full of big changes: marriage, children, job changes, and relocations. What professionals often underestimate is the influence that these life changes can have on your taxable income. For instance, your marital status can impact the value of the deductions you can claim, and your employment status can influence the tax bracket you fall into. The IRS recommends revisiting your W-4 form on a yearly basis to retain control over your finances and potential tax liability.

6. Not Maxing Out Deductible Contributions

What seems to have become a buzzword, and rightly so, are deductions. We are revisiting this due to their sheer utility, although taxpayers seem to have forgotten them. When used correctly, tax deductions can considerably lower your taxable income, and therefore your tax bill. This is particularly useful while planning for your retirement, since contributions to 401k and IRA accounts are tax-deductible, hence affording taxpayers the twin benefit of smaller tax bills and growing nest egg.

7. Not Claiming Applicable Credits and Deductions

While deductions lower taxable income, credits lower tax bills. Both are incredibly useful in maximizing returns when harnessed strategically. Tax credits such as the Child Tax Credit, Kiddie Tax Credits, and Other Dependent Credits lower tax burdens. Additionally, proofs of payments towards loans, fees, charitable donations, and state taxes among others do the same. Most taxpayers fail to take note of where their money is going throughout the year, and then miss out on the opportunities to reap the benefits owed to them. It’s important to remember that the IRS cannot assume anything about your expenses and lower your tax bill in good faith. Getting sizable returns depends on what you declare and claim.

8. Not Filing Online or Asking for a Direct Deposit

The IRS is still battling large backlogs with skeleton staff amidst ongoing legislative changes, and hence urges taxpayers to file their returns online and opt for a direct deposit. Doing so will quell mounting frustration from both ends, and will quicken the refund process. Those who file electronically and provide their bank details can expect their accounts to be credited within 21 days of submission. Of course, it could take a little longer for those who have claimed credits that are prone to be misused (such as the Child Tax Credits), simply due to more stringent verification procedures.

9. Not Consulting a Professional

There is a reason we don’t self-medicate when we’re sick, a reason we don’t fiddle with our cars when it has broken down, and opt instead to visit a doctor or a mechanic. There is an implicit understanding and trust in the professional we choose to consult. We believe in their expertise and heed their advice.

There is no reason the same logic should not be followed when it comes to something as important as filing your taxes, especially when you’re dealing with tax returns in the US as a foreigner.

AOTAX is just the professional team you need: with over 15 years of experience, we’ve taken care of the finances of countless Indian IT professionals. We’ve helped ease tax burdens and made year-round tax preparations much easier. If you’re going to trust a professional, trust AOTAX and sign up for free today!

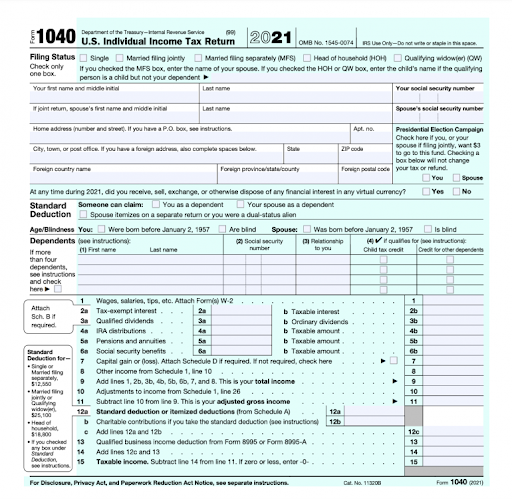

March has arrived, and you have more than 40 days to file your income tax forms. After that, it’s time to pay the IRS and claim certain tax credits/refunds. If you are an Indian citizen in the United States or a US resident, we can show you how to fill out the 1040 form in simple steps.

1040 is a tax form used by United States residents to file their federal income taxes annually. Hence, it’s essential to know how to fill out 1040. The form aids in calculating annual income and the claim on deductions and tax credits.

There were multiple variations of 1040 before 2017. However, since the passage of the Tax Cuts and Jobs Act (TCJA) in 2017, most Americans have been filling out 1040 forms.

Senior citizens can file Form 1040-SE, while non-residents must file Form 1040-NR.

To complete your 1040 form, you have two options:

You can either file electronically, known as e-filing.

Alternatively, you may print the form, fill it out, and mail it to the IRS (Internal Revenue Services).

Compared to manual filing, e-filing is simple, convenient, and quick. In addition, when you e-file your tax returns, you can receive your refund faster. Physical or paper filing takes longer to reach the IRS and delays the refund process.

How to Fill Out a 1040 Form?

Don’t be intimidated looking at the form. Trust us; it’s not that challenging. We provide a step-by-step guide (on the same flow as it is on the form) on how to fill out 1040:

Filing status: It’s essential to specify whether you’re filing your 1040 as a single person, a married couple, filing jointly, or filing separately with your spouse. You can also mention if you are the head of the household or a widower. This will help you take advantage of certain standard deductions based on your status.

Personal information: Fill in your full name, address, and social security number in this field. Whether filing jointly or individually, you must also include additional input about your spouse and dependents.

Election contribution: There’s a neat box in the form that now allows you or your spouse to contribute $3 to the presidential election fund. The money will be equally split between Democrats and Republicans. It would not affect your tax refund or liability.

Cryptocurrency: There is a rise in digital or cryptocurrency as a preferred investment mode. For instance, 46 million Americans are among 300 million cryptocurrency users across the globe. As a result, this feature enables you to declare if you have exchanged cryptocurrency in the previous financial year.

Standard deduction: Your standard deduction eligibility is based on your age, filing status, and whether or not you are blind. Fill in the boxes as applicable. Those who are married and filing jointly with their spouse should also mention if they are financially dependent on another. And if you’re a dual-status alien, you should also mention this in the form.

Dependents: In this section, you may fill in the details about your dependents and seek a tax credit. In this section, you should list your dependents, age, and their relationship with you. You should also mention if you are entitled to a child tax credit or a credit for other dependents.

Calculate taxable income: This section is crucial, and you must fill it in properly. Here is where you list the fruits of your labor from the previous year. This column is where you disclose your earnings from your job. If you are a salaried employee, provide a W-2 form.

Next, simply tick boxes that show your non-employment income, like earned dividends and interest, annuities, pension, IRA tax rebates, social security benefits, and so on. You can find a list of many other deductions on the IRS website.

Calculate your tax liability: Now is the time to count your blessings in the form of tax credits. These are the taxes withheld by your employer. Subtract the tax credits from the total amount you must pay.

The tax bill is the final number. If your tax bill exceeds your tax credits, pay the IRS whenever you file your tax returns. You will receive a refund from the IRS if you have overpaid. If you e-filed, your refund will be directly deposited in your bank account. Otherwise, the IRS will mail you a check.

Schedules

To file your income tax returns, you need a simple 1040 Form. There are separate schedules you attach with 1040 in case of additional income, or if you owe the IRS more money, or you would like to claim extra credit.

These schedules are as follows:

Schedule 1– Fill this schedule if you have earnings from:

A business (also file form C)

Alimony payments

Agricultural income

Educator expenditures

Rental income (file form E)

Health savings account

Health insurance,

Retirement contribution deductions

Student loan or other sources

Schedule 2 – Fill this if you owe the IRS:

Self-employment tax

Alternative minimum tax (AMT)

Household employment tax

Net investment income tax

Additional Medicare tax

Recovery rebate credit because you did not receive a coronavirus stimulus check, an economic impact payment.

Schedule 3 – Use this schedule to claim IRS credits and payments. This includes:

Foreign tax credits

Child and dependent care credits

Education

General business incentives

Home energy credits, etc.

Those who cannot file federal tax returns by April 18, 2022, can request an extension and file by October 15, 2022. If you must make payments, do this before the April deadline.

Back taxes: If you owe the IRS money for previous years’ taxes, you must send 1040 to the IRS. In this scenario, e-filing is not possible.

Refunds: After the IRS processes your returns, you will receive your refund in 21 days.

If you follow the instructions given above, you will be able to file your taxes in no time. If you have all of your receipts and supporting documentation, you should be OK.

If you are an Indian resident in the United States and are unsure how to fill out 1040, contact AOTAX. Our team of capable tax advisers and preparers at AOTAX can assist you in meeting your deadlines smoothly.

Of course, being your boss comes with its perks: Flexible working hours, flexible deadlines, control over your career trajectory, etc. However, those aren’t the only perks of a sole proprietorship. Running a one-person show has more advantages than you would expect.

For starters, it’s straightforward to set up. Low startup costs and no need for a formal structure make it simple to set up such a business entity. In addition, most individuals who have their own business don’t even know that they are considered sole proprietors by the IRS.

Secondly, if well-understood, tax preparation, and filing become much more straightforward when filing as a sole proprietor. For instance, in a sole proprietorship, there is no distinction drawn between your business and yourself.

In simple terms, you are considered both business and individual for tax purposes. In technical terms, this is known as a ‘pass-through’ entity—all business income passes through to the business owner.

Of course, this is taxable and must be declared in the individual’s tax return.

Who Is Likely to Be a Sole Proprietor?

Sole proprietorships generally do not require much in terms of brick-and-mortar start. Therefore, becoming an individual business owner can be easy.

Sole proprietorships are dominated by professionals who can work remotely or travel to customers. Common professions under this type of business formation include:

Freelancers (photographers, web developers, copywriters, editors)

Business consultants or public speakers

Professional cleaners and organizers

Home healthcare service providers (physiotherapists, personal trainers, at-home radiology services)

Landscapers, etc.

What Sort of Taxes Do Sole Proprietors Need to Pay?

As a one-person team, sole proprietors are both bosses and employees. This means, when filing as a sole proprietor, there are a few additional taxes that you need to pay over and above your income taxes.

Sole proprietors are responsible for paying:

Federal and state income taxes

All sole proprietors must declare their business’ profits and losses, as well as any other personal income. The IRS will decide tax brackets and tax bills based on the combination of these two factors.

Self-employment taxes

If you were to work for an employer, you would have to withhold a certain amount of your pay, which is meant for FICA taxes (Social Service and Medicare). However, being your own boss means that you can make these contributions while paying your taxes.

Federal and state estimated taxes

When employed in an organization, employers withhold taxes from your paycheck for you. On the contrary, as a self-employed individual, you must budget for estimated taxes owed for your business and pay them throughout the year. Ideally, you should estimate the total tax bill for the year, and make quarterly payments as required by the IRS.

Which Deductions Do Sole Proprietors Qualify For?

Like any other organization, business expenses are deductible and can reduce your tax bill. Therefore, keeping separate checkbooks for business and personal expenditures is a good habit to follow.

As long as you have accurate and detailed records of the money spent for profit, you can claim deductions for the following:

Automobile and transport expenses

If you depend on your vehicle to keep your business running, you can deduct some of the expenditures you make to commute. You could choose to claim deductibles using either the Actual Expense Method or the Standard Mileage Rate.

Start-up costs

Once your business is functional, there are many operational costs that business owners must incur to keep doors open: repairs, advertising, office supply purchases, and utilities.

These expenses can be deducted from your taxable income up to a limit of $5,000 for the first year you’re in business. After that, any remainders can be removed over the next 15 years.

Professional and legal fees

Seeking professional help from lawyers, accountants, and consultants comes with hefty fees. Luckily, such services are deductible as long as you can provide a receipt and proof of service done for your business.

Insurance

You can deduct any premiums paid toward insurance for health, property damage, loss from theft, etc., from your taxable income. This falls under the ambit of a business operating expense.

Courses for continuous professional development

You may need to upskill from time to time to continue running your business. Therefore, any educational fees paid toward courses that enhance professional abilitiesare tax-deductible.

Apart from the documents required for your tax filing, the following are required:

Form 1040, Schedule C

You must fill the Schedule C, Profit or Loss from Business (Sole Proprietor) of Form 1040. The Schedule consists of five parts:

Part I: Income,

Part II: Expenses,

Part III: Costs of Goods Sold,

Part IV: Information on your Vehicle,

Part V: Other Expenses.

Business owners should keep the following handy:

Business Income Statement

Mileage records (if you plan on claiming deductions for the use of your vehicle to do business)

Inventory count and valuation (if you sell any sort of product)

Records and receipts of all expenses

Schedule SE

If your business earned more than $400 worth of revenue in the year, as a sole proprietor, you must report and pay your FICA taxes (Social Security and Medicare).

Consulting a Tax Professional

Financial advisors can help you set goals according to your business needs while maximizing your tax savings. For instance, you may want to consult a professional to help you prepare for filing as a sole proprietor—-and AOTAX is the best out there for Indian professionals.

With close to 20 years of experience, we at AOTAX are well-versed in US taxation laws and how they apply to Indians working in the US. Therefore, we can help you optimize your tax strategy in the best way possible. Sign up for free today!

Recent Comments