Are tax filing woes quickly becoming the bane of your existence? Have you let the financial year pass by without considering your potential tax burden and how to alleviate it? Unfortunately, many individuals fall prey to last-minute scrambling when it’s often too late to make any changes.

As H1B visa holders, Indian professionals are taxed the same way as US citizens and can claim certain deductions and credits. However, lowering your tax bill is not as simple as it seems.

Efficiently managing your finances requires the implementation of tax planning strategies. These strategies, if well-timed and well-executed, help individuals avoid tax penalties.

The road to filing taxes is long and necessitates constant vigilance and planning all year long. We take you through some essential tax planning strategies for individuals to implement them to make tax season easier.

You can effectively forecast and plan financially toknow which tax bracket you fall into. It is essential to understand that the United States has a progressive tax system—taxable incomes are usually not the same as your total income.

The difference is determined by, and due to, your filing status and the deductions you claim. Hence, the strategies you implement will also be determined by your taxable income figure.

2. Documentation: know what to keep and what to throw

Undoubtedly, the most critical component of tax filing is organized documentation. Having a record of expenditures and statements for the current financial year is as essential as having copies of previous tax returns that date back at least three years.

Why? The possibility of audits. The IRS has three years to decide whether to audit an individual or not. For Indian H1B holders who are taxed on their global income (income earned from investments back home), tax filing should be treated with extra caution, and documentation must leave no room for ambiguity.

3. Tax savers: deductions and credits

Tax deductions and credits are powerful tools and can significantly reduce tax burdens when used correctly. Deductions lower your taxable income, while credits reduce the tax value itself, giving you a larger refund. Below are some of the most popular ways to use these tools to get a more significant tax break:

Retirement planning

Growing your nest egg for retirement while reducing tax bills may sound too good to be accurate; but individuals can maximize savings by making contributions to retirement funds.

Whether you choose to participate in 401k or IRA plans, all contributions up to $6,000 for those younger than 50 lower your taxable income.

Kiddie taxes and child tax credits

For individuals with kids, children’s unearned income (investment-type income) above $2,200 must be taxed using their tax rates, and parents are advised to take note of the same.

Additionally, parents could claim child tax credits on their taxes, which means receiving up to $3,000 per qualifying child above the age of six and up to $3,600 for kids under six.

Educational expenses

Tuition fees, supplies, and other expenses made on classes or courses that improve skills related to your job may be deducted from your taxable income, thereby saving you money.

Health insurance and medical expenses

Medical bills can be financial drainers. So while filing for 2021, make sure to itemize all expenditures that are greater than 7.5% of your adjusted gross income, as they can be tax-deductible.

State income and local tax deductions

Individuals can deduct amounts paid either toward state income taxes or local and sales taxes from their taxable income. The deduction is capped at $10,000 and provides a sizable tax break.

‘Other dependent’ credits

Aside from claiming credits for dependent children, individuals also have the option of claiming credits up to $500 for anyone they may be supporting financially.

Flexible spending accounts & health savings accounts

FSAs and HSAs are valid accounts to have, especially when taking care of your health. So catch up on doctor’s visits, and don’t let your FSA balance go to waste.

As for HSA’s, contributions up to $3,600 for individuals are tax-deductible.

4. Reevaluate filing status and change tax withholding allowances

The IRS recommends yearly tax withholding allowance adjustments to ensure the taxes withheld from your paycheck are best suited to your current needs.

Revisiting your W-4 to check filing status and tax deductions might be a good idea if you’ve experienced any of the following the past financial year:

Getting married

Having children

Unemployment

Salary increments or reductions

Changing jobs

5. Harvest losses

This year, it may be profitable for individuals who jumped on the investment bandwagon to minimize capital gains. You can do so by offsetting gains with losses worth up to $3,000, thereby reducing your taxable income.

6. Donate to charity

Charitable giving is a noble action, and individuals are further incentivized to continue since donations are tax-deductible. Any donations made to a 501(c)(3) registered charity are deductible.

For 2021, there are no limits placed on the number of cash contributions made for those that itemize their deductions. For individuals who claim a standard deduction, the deductible is $300.

7. Work with a professional

Organizing and optimizing your tax returns is no easy task, especially when there are so many things to consider being an H1B holder.

However, handing over the reins and collaborating with seasoned tax planners and professionals can make all the difference to how much money is put back in your pocket.

Having the right people analyze your finances helps you make more intelligent and strategic decisions all year round, and we at AOTAX do precisely that.

Our team has been in the business of assisting Indian IT professionals for close to twenty years. You can trust us to help you get the best returns. So sign up for free today!

An IT job in the US comes with an H1B visa and income in dollars. But it soon loses its charm when it comes down to income tax filing. As per estimates, H1B visa holders nearly pay 35% – 40% of their gross income as various taxes – federal, state, and local. (How much tax do H-1B holders pay? – Greedhead.net) Hence, to cut down your losses and maximize your savings, it is important to have a tax planner by your side that will help you be tax compliant and reduce the tax burden.

While filing your income tax returns (ITR), you can choose between a tax preparer and a tax planner (advisor). A tax preparer will help you with your immediate income tax filing. While a tax planner can help you with your taxes in the long run.

Job of a tax planner:

Everyone has financial aspirations they strive to achieve for themselves and their family. Some want to buy a house, save for retirement, children’s education, or build assets to enjoy during their sunset years. An efficient tax planner understands these goals, analyses their feasibility, and draws out a financial plan to achieve them. They ensure that you fulfill your ambitions without defaulting on your tax payments with the Internal Revenue Service (IRS). They help reduce your tax liability, maximize your tax credits and build wealth accordingly. If you hire a good tax planner you can build assets that you and your family can enjoy.

Qualification:

A tax planner is an expert in their field and knows taxation laws. They are aware about the latest tax laws and procedures. They are also Certified Public Accountants (CPA) in general tax planning or is a specialist in a specific area of tax laws. They are not subject to any state or federal regulations.

Services A Tax Planner Offer

Apart from income tax filing, a tax planner offers you the following services:

They provide financial advice to reduce your tax burden in the years ahead.

They advise on how to maximize your income with appropriate tax savings.

They give advice on financial issues like buying a home, retirement savings, etc., which will help you save taxes.

They help when you get in trouble with the IRS over a tax issue.

Six Steps To Choose A Tax Planner For Income Tax Filing

By now, you have an idea of your financial goals. Now its time for you to choose a tax planner who helps you achieve all this without breaking a sweat. Here is a fool-proof 7 step plan to choosing a tax planner:

1) References: Choosing the right tax planner is essential to have a smooth income tax filing experience. It also makes your life hassle-free all year-round instead of just January-April. The easiest way to find the right tax planner is to ask friends and relatives. You can ask your H1B visa-holder colleagues to give you some references.

2) Check credentials: Once you have found a planner you think is right for you, ask them for some references and credentials.

3) Experience & expertise: Relevant experience matters when you are caught on the wrong side of the taxation laws. Look for a planner whose resume has the number of years they spent in the field managing the IRS. Find someone whose specialty is handling niche clients. For instance, AOTAX has spent 15 years helping over 2 lac Indian H1B visa holders plan and file their income taxes. They are a team of tax planners and advisors who have helped their clients maximize their tax savings.

4) Multi-tasker: Look for someone who can not only be your trusted financial advisor but also a tax preparer. They will help you create wealth as well as file your ITR on time.

5) Check for complaints: This step is important and saves you a lot of time. Check with the Better Business Bureau if there are any complaints of fraud against the advisor if they are also a tax preparer. You can even check with the American Institute of Certified Public Accountants (AICP) if the tax planner/advisor is being investigated for any complaints.

6) Fees: Be clear about the fees you will pay them for their services. Most planners charge a percentage of your asset in question.

7) Ethics: Being ethical is important when you pay your taxes. If a tax planner suggests dubious ways to save tax then that isn’t right. If they suggest to over or under-report your income, claims dependents when you are not eligible, that is a red flag.

With these steps, it is possible for you to easily hire the best tax planner and pay your dues. Plus you can also make the most from your current income.

If you are an H1B visa-holder from India looking to file your income tax returns in the US while saving some extra dollars, do get in touch with us on AOTAX.com. Our team of expert tax planners can easily meet your financial goals. Recommended: What Makes AOTAX the Most Preferred Tax Assistant in 2022

People spend hours pondering over taxes at some point in time. It is upsetting that taxes add to the already busy lives. However, you can make the job a lot easier with a good tax consultant.

In this blog, we’ll unpack the advantages of AOTAX over other tax consultation services like TurboTax or Taxfyle, especially for Indians residing in the US.

Taxes Can be Taxing!

There could be a lot of confusion surrounding income taxes, especially if you are a professional en route to making it big in the United States. However, with Advantage One Tax Consulting Inc., or AOTAX, you will get a complete idea of tax returns, planning, and more.

While tax assistance service providers may promise easy tax preparation without complications, not all are reliable and easy on the pocket. Here is where AOTAX becomes different from Turbotax and Taxfyle.

Rather than making promises of an all-encompassing service package, we curate dedicated human assistants to study your tax documents and check for discrepancies.

While technology fairs over the human brain, the latter does not fall into the many pitfalls that automated tools and calculators are prone to.

Why AOTAX Should Be Your Preferred Tax Partner in 2022

Read on to learn what sets AOTAX apart from other consultants:

1. AOTAX treats individuals and businesses alike

AOTAX is a wholesome service tax consultation company that prioritizes individual customers as much as we focus on businesses. Filing taxes and maintaining financial documents is as difficult for individuals as for small and big businesses. Therefore, AOTAX assigns qualified professionals to guide you through this hectic process.

As an NRI, you may find it exhausting to look through the nuances of tax filing in the US. Even if the country does not recognize you as a tax resident, you can file income tax returns as an employee in accordance with the provisions permitted by the firm you work for. Our professional team offers Tax Return services, ITIN Guidance, FBAR & FATCA Processing services, and more!

If it is payroll processing that your business is struggling with, like 35% of companies registered with the Electronic Federal Tax Payment System (EFTPS), AOTAX has got your back!

2. AOTAX is 100% online and manual checks for enhanced accuracy

AOTAX is specific about assigning individual experts to curate tax details for customers at the backend. Even though we offer a completely online interface to interact with you, your work would be done by expert human analysts – not automated software.

With the help of our professional team, you can easily file tax returns online as well. Starting from January 24, 2022, you can file tax returns online even if you are not a tax resident. You could qualify for a refund or tax credit later.

Filing taxes online is a more convenient option. Read about its convenience here. However, if you are doing it for the first time and have hesitance using such software, we advise you to consult our expert team, who can guide you through it all online.

3. AOTAX focuses on tax planning

Preparing taxes is a one-time job that occurs between January and April. It essentially analyzes many documents surrounding your income and investments, as well as retirement strategies. A Certified Public Accountant or CPA is responsible for preparing your taxes.

However, tax planning is a future-centric process that studies how to minimize taxes in succeeding years and prioritizes savings. Brands like Turbotax and Taxfyle often compromise this. Tax planning involves the analysis of your financial behavior to manage taxes and maximize returns.

At AOTAX, you can customize a personalized strategy for you and your business to improve your tax returns and invest wisely. In addition, AOTAX is a tax planning consultant that makes it a point to hold regular meetings at your convenience to help you chart your finances by your objectives, future aspirations, and values.

4. AOTAX doesn’t promise impossible returns

AOTAX is a practical tax planning partner. We focus on not pestering clients with unwanted upgrades and false promises. Perhaps the most nagging aspect of consultant agencies is offering recurrent and utopian promises, but we associate with clients transparently and plausibly.

Whether your business needs assistance or yourself, AOTAX can develop a comprehensive financial statement for you, encompassing a strategy for you to follow for maximum returns. If your business needs our service, we will represent you at tax audits and meetings to give it maximum exposure and successful leverage.

However, we don’t guarantee overnight miracles. Instead, we promise continuous assistance and complete confidentiality. Rather than presenting a common plan for every customer, AOTAX focuses on curating customized options for you according to your needs. This is how we differ from Turbotax and Taxfyle.

5. AOTAX offers audit defense and services

While many consultants do not have a standard tax audit service, AOTAX offers it as a standard among our many other packages. Take a look at our services that include financial planning and audit defense. If you are struggling under the weight of tax debt, AOTAX can offer resolutions to pick you up from your financial mayhem.

Our team takes into consideration your financial capabilities and constraints alike before designing a strategy for you and your business. We do not make it heavy on your pocket by asking for recurrent charges. Instead, our tax advisory service can mold a plan for your entire future, including your retirement.

Moreover, we don’t push for unwanted upgrades.

Choose us Today

From individual services to business strategies, AOTAX can be the savior you were in search of. Do not give in to the pressures of your host country, and reach out to us today. We will walk you through the details of everything tax-related in the US.

FBAR & FATCA Processing, ITIN Processing, Extension Filing, and Tax Return Services offered by AOTAX have abundantly secured the lives of many US-based Indians since 2003! This sets us apart from other consultancies that contain empty words and confusing workflows. We make it easy, convenient, and fast for you.

It is time for you to let go of complex and conventional tax solutions offered by firms like Turbotax and Taxfyle. AOTAX makes the process breezy!

Taxes received from citizens are a country’s principal source of revenue. In India, too, the income tax collected accounts for most government revenue.

If you’re an Indian IT professional having links to the US, you may be required to pay income taxes in the United States even if you are not a U.S. citizen. Whether you should file a tax return in the United States is determined by whether the US government deems you a “tax resident.”

Although paying taxes in both countries is sometimes necessary, the two nations have treaties to safeguard NRIs, such as the Double Taxation Avoidance Agreement. Tax planning for Indian IT professionals need not be tricky when you know the nitty-gritty of the same.

Immigration and Taxes: Who Has to Pay Taxes?

In terms of taxes, the United States divides people into two categories: tax residents and non-tax residents. You may be asking how to figure out how immigration and taxes apply to you if you have recently immigrated to the United States?

Even if you are not a US citizen, you may be obligated to pay US taxes in different circumstances. Whether you must file and pay taxes is determined by the government’s classification of you as a tax resident.

However, not all non-immigrant visa holders are tax residents, though. Even if you are not a tax resident, filing an income tax return if you have worked for an employer who withholds taxes from your salary is a good idea since you may be eligible for a refund.

Non-immigrant visa holders can only become tax residents if they stay in the United States for at least 183 days in the current year. For example, if you spend 200 days in the US and have a non-immigrant visa, you must report your earnings to the Internal Revenue Service (IRS).

Furthermore, even if you spent less than 183 days in the United States during the current year, a weighted system could classify you as a tax resident.

Unless you spent less than 30 days in the United States during the current year, you are a tax resident if you have spent at least 183 “weighted” days in the US during the previous 3 years.

This means that if an NRI works in the United States and earns money from India, he is only liable for US taxes. For this purpose, the person must present a US IRS-issued Tax Residency Certificate to his Indian payee. If taxes were deducted in India, the NRI could file a tax claim in the United States for that amount.

NRIs’ income received in India is taxed differently in the United States, depending on their taxation policies. The following are the criteria on which NRI taxation in the United States may be imposed. This can help in tax planning for Indian IT professionals.

1. Income from salary

In India, if an individual receives a pay package with multiple components, each component is taxed separately. Individuals may also qualify for tax breaks or exemptions if they get medical reimbursements or allowances.

In the United States, however, the same taxing conditions do not apply to salaries. An individual’s income is taxed regardless of how much the person earns.

The taxable components of your salary are listed on the well-known Form 16 in India. In contrast, if an individual or NRI files an ITR in the United States, all tax-free components of the pay received in India must be disclosed. At the same time, these individuals must pay taxes on those components in the United States.

NRIs must use the tax return Form 1040 to report their salary income in India. Form 1116 is used to file a tax return or claim a tax credit.

2. Freelancing and contractual income

This is applicable for NRIs who provide consulting services in the United States but earn money from India. In this case, the linked NRIs are taxed in the United States on that income. Therefore, whether the income is received in the United States or an Indian bank account, this tax must be paid.

The provisions of the DTAA, or Double Tax Avoidance Agreement, must be considered in this case.

3. Rental income

If an NRI rents an Indian property, his rental income will be taxed in the United States. Any rental income from immovable property may be taxed in the country where the property is located, according to Article 6 of the DTAA.

As a result, any income from rent in India is subject to taxation for US NRIs. NRIs, on the other hand, must declare this income while submitting their US tax return. Taxes paid in India would be credited to them.

It’s worth noting that salary and contractual income are only taxed in the country where they’re earned. Both countries, however, have the option of taxing rental revenue.

The first right belongs to the country in which the property is located. As a result, the NRI will pay tax on his rental income in India first, according to his available Indian tax slab.

The rental income must then be declared by the NRI taxpayer in the United States. The tax on his entire income is then calculated using his tax bracket in the United States. The NRI might claim a tax credit in the United States for whatever taxes he paid in India.

NRIs in the United States must file Form 1040 Schedule E for tax purposes. In India, rental income is subject to a 30% tax reduction. Actual expenses, such as maintenance and repair, are deducted in the United States. Form 1116 tax credit claims must be completed.

4. Income from the sale of agricultural land

In India, the selling of agricultural land is a tax-free transaction. It is, however, taxed in the United States. An NRI’s income from the sale of agricultural property must be declared in the United States and taxed as part of their global income.

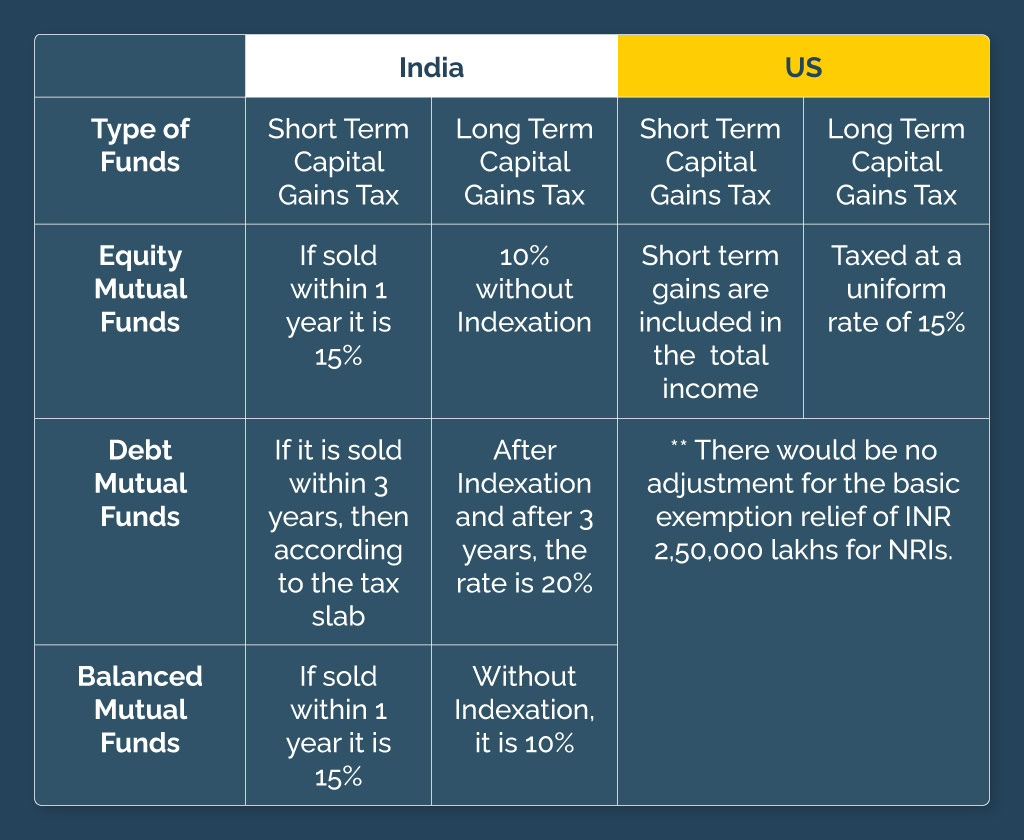

5. Capital gains

A capital gain is any profit earned from selling capital assets such as land, property, stocks, shares, mutual funds, etc. In India and the United States, the time period used to establish whether an asset is a long-term or short-term capital gain is different. NRIs face new challenges because of this.

It may result in NRIs paying tax on their sales in India and additional tax on the remaining amount in the US, notwithstanding the possibility of claiming the tax credit in the US. To an NRI, this could result in a double taxable asset.

Long-term capital gains in the United States are taxed at the same rate for all assets, one year. Long-term capital gains are taxed at a rate of 15%, whereas short-term gains are added to your total income.

The following table summarizes the above topic of capital gains taxes:

6. Income from interest generated

Interest income is added to the total income of each Indian resident and then taxed according to the overall tax bracket. This is usually 30% percent of the interest income.

Interest earned in India or the United States is added to the NRI’s total income and taxed according to the bracket in which it falls. This may be different in the United States, depending on the state’s legislation where the NRI resides.

If an NRI earns interest on deposits in India, he will have a tax deduction of TDS in India at a reduced 15 percent rate if the DTAA is in place.

7. Income from dividends

In India, any dividend income is tax-free. On the other hand, Dividends are added to total income and taxed in the United States.

NRIs must report “Interest and dividends” income on Schedule B of Form 1040 to be taxed. Foreign tax credits can be claimed using Form 1116.

8. Foreign Tax Credit Limit in the USA

In the United States, NRIs can claim a tax credit; however, the IRS has set a limit. For this, you’ll need to fill out Form 1116. This means that the foreign tax credit should be calculated in accordance with the NRI’s US tax due in the same proportion as the NRI’s total income.

It’s important to realize that taxes in the United States differ from state to state. As a result, the taxes paid by NRIs in different states vary. The above criteria for NRI taxation can help in tax planning for Indian IT professionals.

Personal tax returns can be a stressful undertaking. AOTAX can relieve you of this burden by preparing your Personal Tax Returns for you.

We are all Registered Tax Agents with vast hands-on expertise, and we all take great pride in assisting our clients in achieving their objectives.

We do everything we can to minimize your tax while making the overall taxing procedure as efficient, easy, and cost-effective as possible, thanks to a staff of highly skilled and experienced Tax Accountants. Contact us if you are an IT professional working in the USA and looking at filing tax in the USA.

People often think of tax preparation when they think about doing their taxes. As tax time approaches, people scramble to find savings and frantically rush to file their returns and avoid incurring penalties. However, a tax strategy is not just for filing your taxes every year. It can be an effective means of planning for the future and minimizing your taxes simultaneously. This is exactly where you need tax planning.

So, then are tax planners different from tax preparers? In a nutshell, yes. The process of tax preparation is reactive, whereas tax planning focuses on the future.

While these words sound similar, each refers to a different aspect of taxation and has distinct meanings. As we go through each service, let’s see how they differ and choose the best one.

What is Tax Preparation?

Preparing taxes is typically a one-time task. Normally, tax preparation takes place between January and April. A tax preparer or Certified Public Accountant (CPA) prepares tax returns before the deadline for filing. Tax preparation needs several documents that provide valuable information regarding income, investments, and retirement plan statements. The approach also considers multiple income streams, deductions, and charities.

The role of a tax preparer

A tax professional prepares the tax return by organizing and entering the previous year’s tax information. So you need to visit a tax preparer once or maybe twice a year. Their expertise in tax laws ensures that returns comply with the IRS regulations. So you can rest assured about meeting the federal and state regulations.

Tax preparers can offer general tax advice and tax-saving suggestions based on your previous records. A tax preparer can address general questions regarding the filing process. There will, however, be no proactive tax strategies to help you reduce your tax liabilities. The reason – Such meticulousness, detail, and planning fall into a more comprehensive process requiring more expertise and attention.

Qualifications to look for in a Tax Preparer

Preparer tax identification numbers (PTINs) are the primary requirement for preparing taxes. A PTIN needs no additional credentials or accounting experience. Some states require tax preparation certification, similar to a PTIN but do not signify expertise or competence. Tax preparation services can be provided for a fee by qualified tax preparers.

While anyone with a PTIN and the required state credential can prepare your tax return, it’s a prerequisite to be either a Certified Public Accountant (CPA), enrolled agent, or an attorney who can address things like IRS issues, payments, audits, and collection activities.

Benefits of tax preparation

Save more money. A tax professional understands tax laws and compliance. They maximize your tax deductions and credits.

Save time. It takes a great deal of time and effort to prepare your tax return independently. A tax preparer can save all that time.

Error-free returns. A mistaken tax return can have disastrous results. Errors can lead to audits and penalties. Additionally, you can reduce your risk for audit with tax preparation.

What is Tax Planning?

A comprehensive tax strategy will help you chart a course of financial behavior that will help you manage your taxes in the future. When it comes to tax planning, it’s less about your specific return and more about how to maximize it.

The role of a tax planning agency or tax planner

Financial planning often entails a regular meeting with a financial planner and taking an active role in making decisions about your finances. Tax planning, on the other hand, is an ongoing process, one that shifts and changes as your goals do. A tax planner or tax planning agency integrates the changing financial dynamics and fosters an open and transparent relationship with its client. A tax planner will analyze your financial objectives, values, and future vision to create a personalized financial plan.

Creating a tax plan that meets your needs and considers your goals is essential. Few tax planning services like AOTAX have specific plans for businesses and individuals. They chalk out a plan considering both business and individual tax needs. The services vary from advisory services to business tax preparation and planning. All that so you can act fiscally responsible and tax-friendly.

Qualifications to look for in a Tax Planner

While tax planners require a great deal of expertise and specific knowledge, they are not subject to any federal or state regulations. They need to hold a CPA for general tax planning or be an accredited tax advisor for sophisticated cases. The biggest asset for a tax planner is their industry knowledge regarding applicable laws and particular situations.

Benefits of tax planning

Reducing tax liability. An individual tax planner or tax planning agency focuses primarily on lowering liabilities or routing investments. When you have business income, planning throughout the year ensures you maximize tax credits, harvest losses from investments, and manage your wealth accordingly.

Flexible estate planning. Don’t just leave your assets, but add a legacy to your heirs. You can lower your own and your heirs’ tax liabilities with tax planning.

Know your investment returns. Your carefully thought-out investment plan can be ruined by expenses, capital gains, and even inflation, leaving you with considerably fewer returns than you anticipated.

Tax Planner vs. Tax Preparer

Tax preparation businesses cannot provide you with the expertise you need for tax planning. Planning your taxes and saving money are two ways tax planners can help you. A tax planning strategy must be implemented year-round to minimize your tax liability.

Tax planners typically offer the following services:

Strategy for harvesting tax losses.

Tax bracket management.

Constantly plan other investment strategies which could get deserved returns while saving on taxes.

Tax preparers typically provide the following services:

File tax returns.

Comply with state and federal tax laws.

Handle missed deadlines and resolution paperwork.

Finally, a tax planning agency is the best solution by weighing the differences. A tax planner will tailor the plan to meet your needs. They care about your individual or business financial goals and plan the future. Their meticulous planning strategies will help you reach those objectives while also fitting the taxation rules. Investing and taxes can sometimes seem out of reach. But not anymore with AOTAX. Get in touch today to get your free tax draft!

Recent Comments