Living in the US with a working visa comes with its share of challenges, and navigating the legal terrain can be difficult, especially when it comes to something as complex as filing your taxes. For all money earned in the United States, H1-B visa holders are subject to US income tax legislation. But things start to get critical when filing for tax deductions.

So we’ve created a comprehensive guide to tax filing for Indian H1B visa holders. Read on to learn more about the process and get through it painlessly.

Frequently Asked Questions about Tax Filing for Indian H1B Visa Holders in the US

Below are some of the most widely asked questions about tax filing for Indian H1B Visa holders in the US:

Who does this taxation apply to?

You’re a highly-skilled professional from a STEM background and fall under the category of ’alien’. You hold an H1B Visa, have permission to work in America for the next three years, and have an employer sponsoring you. Ahoy! You are now subject to paying taxes on your income at the same rate as any other US citizen or resident.

However, it’s not quite so simple. To be considered a US resident for tax purposes, the Internal Revenue Service (IRS) relies on the additional criteria of physical presence in the country to determine whether a migrant in the workforce is liable to file taxes. What is known as the Substantial Presence Test (SPT) is used to determine eligibility and comes into effect on a calendar-year-by-calendar-year basis.

To pass the test, an individual must have been present in the US for at least:

31 days of the current calendar year and,

183 days over the current year and the two years preceding it. More specifically, this count must include all days in the current year, one-third of the days present in the year before the current year, and one-sixth of the days present two years before the current year.

To illustrate, let’s look at the hypothetical example of Suresh, a software engineer who moved to the US in the year 2019.

Suresh has been physically present in the US for 180 days during the 2019-2021 period and would need to count 180 days for the current year (say, 2021), 60 days for 2020 (⅓), and 30 days for 2019 (⅙). Totaling up, Suresh has 270 days of physical presence in the US, which is more than the minimum required to qualify as a resident for tax purposes.

Of course, there are specific guidelines regarding what counts as a day of presence. You can read more about this on the official IRS website.

How much will I be taxed, and which taxes would I have to pay?

H1B taxpayers can expect to lose anywhere from 20% to 40% of their incomes to federal, state, and local taxes, but this depends on income levels and appropriate deductions. These taxes include:

Federal Income Tax

The taxes charged on your US income as a nonresident H1B holder depend on marginal brackets that vary as per your income. Although tax values are the same as those for US citizens and residents, H1B nonresidents will not qualify for the deductibles available to citizens. You can find out more about an estimate of your tax bracket here.

Medicare and Social Security (FICA)

Roughly 8% of your income will be deducted and paid towards your Medicare (1.45%) and Social Security (6.2%), each of which will be matched by your employer. In addition, employers are liable to pay the same amount on your behalf to the IRS, which secures provisions for pension funds, among others.

State Income Tax

Depending upon the state you live in, the tax you pay could range from 0% to 10% of your income. Some states such as Washington, Texas, and Nevada levy no additional charges, while states like California mandate employers to withhold roughly 7% of employee incomes for taxes.

Local Income Tax

Similar to State Income Taxes, towns and cities may levy additional taxes, and employerscould deduct up to 4% of your income for the same.

Am I eligible for any tax benefits?

H1B Visa holders cannot claim the same tax benefits, credits, and exemptions as permanent residents and citizens.

Preparing the required documentation can be a daunting task, but the general rule of thumb stipulates keeping the following handy:

Photo ID.

Social Security number.

Valid wage documents and earning statements from all employers in the last financial year (form W-2, W-2G, 1099-R,1099-Misc).

Receipts for relevant deductions.

Documents related to name changes, dependency, and relocation due to marriage for married individuals.Tax Filing for Indian H1B Visa Holders in 2022 – Next Steps and the Road Ahead

Tax Filing for Indian H1B Visa Holders in 2022 – Next Steps and the Road Ahead

Tax season is approaching, and filing doesn’t happen overnight. How should you prepare?

Step 1: Check your eligibility

Take the SPT, and make sure you meet the requirements for days present in the country.

Step 2: Get organized

Gathering documents and getting them in order takes longer than you think it would. So to make tax filing as seamless a process as possible, make sure you have everything ready to avoid last-minute scrambling. This, of course, means being aware of deadlines and being prepared well in advance.

Step 3: Find professionals who can help you

Taxes are confusing at their best and daunting at their worst – especially for Desis in a foreign land. Getting the best returns possible requires the technical know-how of qualified professionals. And at AOTAX, we’ve been helping our fellow Indians file their taxes in the US for over a decade.

We offer:

Tax planning advisory, return, and preparation services. We also help with extension filing and ITIN and FBAR FATCA processing.

Easy access to an online portal, and free sign-up for new customers.

Filing tax returns can be tricky, confusing and you ought to be cautious while filing your tax returns.

So, let us give you some basic tips to follow while filing your tax returns. These tips will help in avoiding common mistakes to ensure that your taxes are filed properly and you obtain the maximum refunds.

1.Filing for an extension

You can easily file for an extension in the timeline of your tax return filing but, an extension in the due date for tax payment cannot be done. You might have the thought that you may end up having taxes to pay once your return filing is completed. So, you should pay whatever amount you owe to the IRS by the July deadline so that you could do reconciliation after the returns have been filed successfully. If you do not pay your taxes by the deadline, you might have to pay a penalty which you should try to avoid.

2.Document your charitable contributions meticulously

Nowadays, charitable contributions are getting a lot of scrutiny from the IRS. So, if you are planning to claim charitable contributions as itemized deductions in your tax returns then you must have written acknowledgment from charitable organizations for contributions made of $250 or more. The contribution made can only be claimed if they are made to a qualified organization. In case of your contribution being less than $250, you must keep a list or record of what you contributed and to whom.

3.Know about new due dates for some tax returns

There might be some information forms that would be needed by you for filing your tax returns might be having different due dates than that of your tax returns. So, you need to be alert and visit the IRS’s website for the information on these new due dates.

4.Need for amendment

Many taxpayers have to file amended tax returns due to reasons like receipt of updated Forms 1099, Schedules K-1, and other information forms later than filing your actual tax returns. You need to be aware of the factor that if you are receiving any rectified information returns ad you have already filed your tax returns then you would not have to amend your returns if the difference is not more than $100 in your income or not more than $25 in your withholding. In these cases, your information and filing both would be considered as correct and no penalty would be charged.

5.Expiry of your ITIN

If you are using your ITIN for tax returns filing, then you must be careful about your ITIN being expired. If your ITIN has not being used for filing federal tax returns once within three years then your ITIN must have been expired and it needs to be renewed. You can renew your ITIN by submission of Form W-7 and the necessary documents as well. If you are filing your tax returns without a valid ITIN or without submitting a renewal application for your ITIN then there might be adjustments made into your tax returns. Your income tax return would be processed but you would not receive the refunds and any exemptions claimed on the income tax return would be denied to you.

6.Disaster losses

In case of any loss incurred in an area that has been federally declared disaster area, the losses can be claimed as an itemized deduction on your federal income tax returns. This loss must be related to your home, your vehicles, or any household items and the amount which you can deduct are reduced by any insurance payment which you have received or reduced by any salvage value of your property. These losses can be deducted on Schedule A of Form 1040 for the year in which the losses have occurred.

7.ID Theft

The tax season is the best season for identity thieves. You must be very vigilant and should try to keep your financial information secure. You should not send your financial information to a tax preparer by electronic medium if the medium is not encrypted. Moreover, you should be careful about phishing scams which can be in the form of fake email, text, or anonymous phone call.

8.Private debt collectors on the job

There has been a relative change in the IRS procedure i.e. the use of private debt collectors for certain federal bills that are overdue. If your tax debt is to be collected by debt collection agencies then you would be notified by a letter that confirms this. The collection agencies would send collectors who can be said as IRS contractors and any check you pay would be addressed to the IRS.

9.Query resolution with the IRS

Your queries on tax returns can be addressed by the Interactive Tax Assistant present on the IRS. This can be helpful for you in resolving your queries and thus, assisting you in filing your tax returns correctly.

10.Selection of your tax preparer

If you are planning to hire a tax preparer for preparation of your tax returns then you must obtain referrals, check the credentials of the tax preparers, interview them, and understand the method they use to bill, etc. These are the vital information that you must collect and you must check if they have a PTIN (IRS Preparer Tax Identification Number) or not which is mandated by the law.

Conclusion

Hence, you can follow these tips and file your tax returns successfully on time without facing any inconvenience or difficulties.

How can a qualified tax professional help you e-file your taxes amidst the pandemic to maximize your refunds?

By hiring qualified tax professionals for your tax preparation, you are free from the stress of preparing the tax returns alone. The expertise of qualified professionals would ensure that you obtain all the deductions and credits which you are eligible to receive. You can gain peace of mind, avoid making mistakes while filing tax returns, and also save your time by hiring qualified tax professionals.

Currently, the pandemic COVID-19 has created mayhem all around and has affected the economic condition of the entire country. Several businesses have been shut down and millions of Americans have lost their sources of livelihood. In such a deteriorating situation, obtaining a considerable amount of tax refund would be very helpful to ease the financial stress for some time.

If you are preparing your tax returns with the help of a qualified tax professional, your tax preparer would suggest you several methods to e-file by which you can obtain maximum tax refunds.

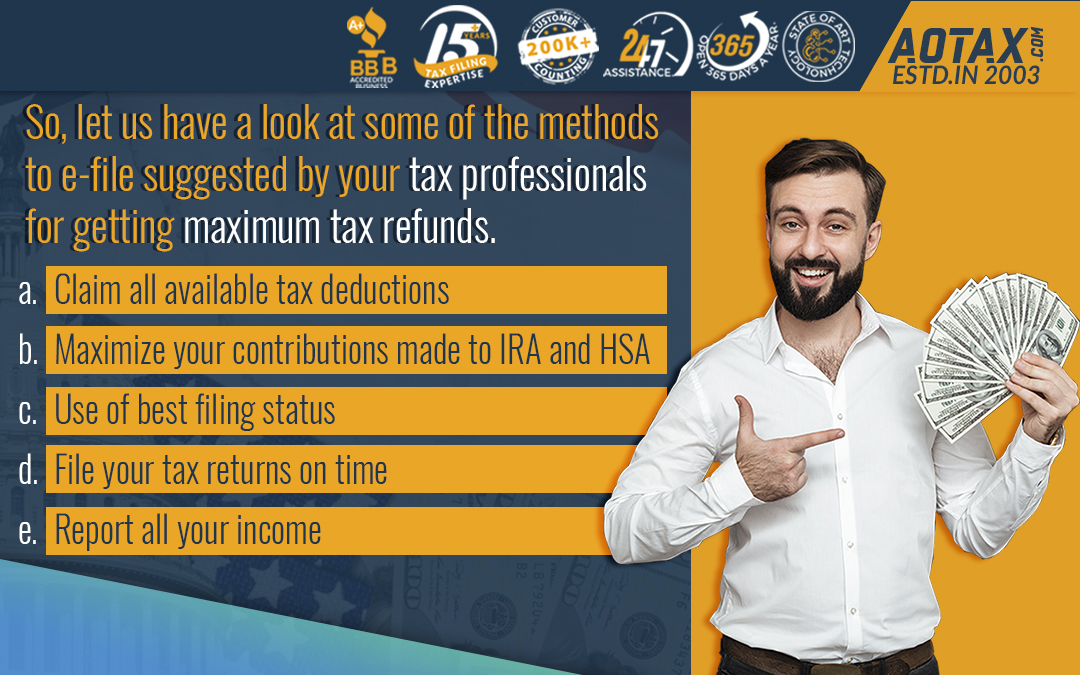

So, let us have a look at some of the methods to e-file suggested by your tax professionals for getting maximum tax refunds.

a.Claim all available tax deductions

Your tax preparer would suggest you to dig into all available tax deductions. There are many common deductions available such as charitable donations, medical costs, interest on mortgage and education expenses, etc. The deductions would be subtracted from your AGI (Adjusted Gross Income) thus, lowering your taxable income. As your taxable income would be low, you would have to pay fewer taxes and you can obtain higher refunds.

However, there are some deductions which you might not be aware of or are very easily overlooked such as State Sales Tax, Student loan interest, Out-of-the pocket charitable contributions, Certain jury duty fees, Child and dependent care, Reinvested dividends, State income tax paid on returns of last year, Earned Income Tax Credit (EITC), etc. You must keep good records of your deductions especially in case of charitable contributions. Moreover, your tax preparer would suggest you to ensure that you are claiming deductions for those organizations which have the status of “Tax-exempt” with the IRS.

b.Maximize your contributions made to IRA and HSA

Your tax preparer would suggest you maximize your contributions which you are making towards the IRA and the HSA. Traditional IRA contributions can help reduce your taxable income. The contributions made towards Roth IRA do not qualify for tax deductions but they can qualify for Saver’s credit if you can meet the income guidelines. In case, you are self-employed you can be able to contribute towards a certain self-employed retirement plan till 15th October 2020.

Your pre-tax contributions to an HSA can also help lower your taxable income. Your tax preparer would suggest you to contribute more towards your HSA before the timelines are closed. You should have enrolled in a health insurance plan which has high deductibles that either meet or exceed the required amounts of the IRS.

c.Use of best filing status

One of the major factors which can maximize your tax refunds is the choice of your filing status. You must inform your tax preparer about any of your major life changes before e-filing. Your relationship status on 31st December of a year determines your entire year’s filing status and you must use it while filing your tax returns. These options for filing status include Single, Married and filing jointly, Married and filing separately, Head of household or qualifying widower. If you could file your tax returns using two statuses such as “Single” and “Head of Household”, your tax preparer can calculate your taxes and find out which one would be beneficial for you in terms of more returns.

d.File your tax returns on time

Your tax professional would always suggest you to file your tax returns on time. This increases your chances of getting a maximum refund. The only exception to this is the case in which you have filed for an extension in the timeline to file your tax returns. The IRS charges penalties for not being able to file your income tax returns on time. Your penalty would be around 5% of your unpaid taxes for each month late up to 5 months from your tax filing deadline. Moreover, if you are not paying your taxes on time the IRS would charge penalties and interest on it. If there are penalties and interest levied by the IRS, then it is quite obvious for you to obtain low tax returns.

e.Report all your income

Many people do not report all income on their return. This can be intentional or unintentional but the IRS would charge penalties for this. If IRS uncovers your unreported income then it would charge penalties and interest on your unpaid taxes. Your tax professionals would suggest you to spend some extra time in reviewing your returns and make sure that you are not forgetting any source of income. Usually, the sources of income that are overlooked are the interest income, income from dividends, contract work, 529 contributions, charitable gifts, etc. You can maintain a spreadsheet and keep on updating your income sources every year to avoid mistakes while tax preparation.

Conclusion

Hence, with the help of these tips and methods, you are sure to maximize your refunds during these difficult times. If there is an error after filing your tax returns which would affect your refund amount, you can amend your return by filing Form 1040X.

All you need to know about Multiple State Tax filing

Multiple state tax filing As the pandemic COVID-19 continues to affect common people in the worst manner, many Americans who were residing in different states for work are gradually returning to their native states. People have now decided to return to their native States and work remotely. So, now you have quite a large number of tasks lined up for yourself.

You need to settle down, make yourself a part of the new community, and obtain a new driving license, register to vote in the new state, and many more. One more additional task is the filing of the tax return. Until now, you were filing only the Federal tax returns but now you would have other tax returns to file. These would include the need to file a tax return in the State you moved from to the State you have moved to.

Queries and confusions related to multiple state tax filing usually arise if you are earning income in different states during the same calendar year. These confusions can occur due to several reasons such as

If you are changing your residency in the mid of a calendar year to a new State.

If you are into a profession where your work makes you present in multiple states in a particular calendar year.

If you own investment property outside your home state.

Determination of State residency

For most the Americans, determination of resident state is quite simple. The complications and risk of being open for a State Audit might arise if your stay time is split between multiple states.

You will have to prove to the State about your residency by showing up things like where you had been living in most of the year, where you own property; your bank accounts are present in which State, where are you registered to vote, etc.

Determination of your State residency is the primary step in the calculation of your State tax as it will help in determining the State in which you would have to file a state tax return as a resident.

Non-resident State tax return

For those non-resident states where you have earned income, you will have to file a Non-resident state tax return. In this form, you will have to report only those incomes which were earned in the Non-resident states.

a. In case, you are the owner of an investment property in the Non-resident State then your tax return to be reported would be rental income minus the associated expenses.

b.If you are a consultant who is working in some project out of the resident state then the income to be reported would be the proportion of your salary earned while you are working on that project.

c.There are some states such as New Jersey and Pennsylvania which are into an agreement by which there is no obligation for the residents of the states to file a non-resident state tax return if they are earning in the non-resident state.

Resident State tax return

In case of your home state’s tax returns, you have to report all income that you have earned which even includes the income that has been earned in different states. This implies that all your income in that calendar year would be subject to resident state’s tax laws.

While you are completing your tax returns, you will have the opportunity to list down the taxes which you owe to pay to other states. This would be applied as a credit against the taxes which are owed to the resident state

and so,you are not in a bad state by making a part of your income outside your resident state.

Part-year resident State tax return

The part-year resident State tax return would be relevant for those Americans who have moved from one state to another in the middle of a calendar year. By this, you would have an opportunity to split your income between the two states and claim to be a resident of both the states.

For the calendar year in which you are moving from one state to another, you would file the Part-year resident State tax return. However, you do not have to worry about paying double of your State tax.

Mostly, states would tax only income earned within the state and not outside the state. When you know the exact income earned in each state, you can easily report the exact income for each state. This can be feasible if you had a savings account in your old state which you closed while moving and opened a new one in your new state.

Conclusion

Hence, filing of State tax returns is somewhat confusing and would take some more time. You must determine your state of residency carefully, understand your income allocation as you cannot take the numbers reported on your W-2, and review your state tax returns carefully.

Recent Comments