An IT job in the US comes with an H1B visa and income in dollars. But it soon loses its charm when it comes down to income tax filing. As per estimates, H1B visa holders nearly pay 35% – 40% of their gross income as various taxes – federal, state, and local. (How much tax do H-1B holders pay? – Greedhead.net) Hence, to cut down your losses and maximize your savings, it is important to have a tax planner by your side that will help you be tax compliant and reduce the tax burden.

While filing your income tax returns (ITR), you can choose between a tax preparer and a tax planner (advisor). A tax preparer will help you with your immediate income tax filing. While a tax planner can help you with your taxes in the long run.

Job of a tax planner:

Everyone has financial aspirations they strive to achieve for themselves and their family. Some want to buy a house, save for retirement, children’s education, or build assets to enjoy during their sunset years. An efficient tax planner understands these goals, analyses their feasibility, and draws out a financial plan to achieve them. They ensure that you fulfill your ambitions without defaulting on your tax payments with the Internal Revenue Service (IRS). They help reduce your tax liability, maximize your tax credits and build wealth accordingly. If you hire a good tax planner you can build assets that you and your family can enjoy.

Qualification:

A tax planner is an expert in their field and knows taxation laws. They are aware about the latest tax laws and procedures. They are also Certified Public Accountants (CPA) in general tax planning or is a specialist in a specific area of tax laws. They are not subject to any state or federal regulations.

Services A Tax Planner Offer

Apart from income tax filing, a tax planner offers you the following services:

They provide financial advice to reduce your tax burden in the years ahead.

They advise on how to maximize your income with appropriate tax savings.

They give advice on financial issues like buying a home, retirement savings, etc., which will help you save taxes.

They help when you get in trouble with the IRS over a tax issue.

Six Steps To Choose A Tax Planner For Income Tax Filing

By now, you have an idea of your financial goals. Now its time for you to choose a tax planner who helps you achieve all this without breaking a sweat. Here is a fool-proof 7 step plan to choosing a tax planner:

1) References: Choosing the right tax planner is essential to have a smooth income tax filing experience. It also makes your life hassle-free all year-round instead of just January-April. The easiest way to find the right tax planner is to ask friends and relatives. You can ask your H1B visa-holder colleagues to give you some references.

2) Check credentials: Once you have found a planner you think is right for you, ask them for some references and credentials.

3) Experience & expertise: Relevant experience matters when you are caught on the wrong side of the taxation laws. Look for a planner whose resume has the number of years they spent in the field managing the IRS. Find someone whose specialty is handling niche clients. For instance, AOTAX has spent 15 years helping over 2 lac Indian H1B visa holders plan and file their income taxes. They are a team of tax planners and advisors who have helped their clients maximize their tax savings.

4) Multi-tasker: Look for someone who can not only be your trusted financial advisor but also a tax preparer. They will help you create wealth as well as file your ITR on time.

5) Check for complaints: This step is important and saves you a lot of time. Check with the Better Business Bureau if there are any complaints of fraud against the advisor if they are also a tax preparer. You can even check with the American Institute of Certified Public Accountants (AICP) if the tax planner/advisor is being investigated for any complaints.

6) Fees: Be clear about the fees you will pay them for their services. Most planners charge a percentage of your asset in question.

7) Ethics: Being ethical is important when you pay your taxes. If a tax planner suggests dubious ways to save tax then that isn’t right. If they suggest to over or under-report your income, claims dependents when you are not eligible, that is a red flag.

With these steps, it is possible for you to easily hire the best tax planner and pay your dues. Plus you can also make the most from your current income.

If you are an H1B visa-holder from India looking to file your income tax returns in the US while saving some extra dollars, do get in touch with us on AOTAX.com. Our team of expert tax planners can easily meet your financial goals. Recommended: What Makes AOTAX the Most Preferred Tax Assistant in 2022

Taxes received from citizens are a country’s principal source of revenue. In India, too, the income tax collected accounts for most government revenue.

If you’re an Indian IT professional having links to the US, you may be required to pay income taxes in the United States even if you are not a U.S. citizen. Whether you should file a tax return in the United States is determined by whether the US government deems you a “tax resident.”

Although paying taxes in both countries is sometimes necessary, the two nations have treaties to safeguard NRIs, such as the Double Taxation Avoidance Agreement. Tax planning for Indian IT professionals need not be tricky when you know the nitty-gritty of the same.

Immigration and Taxes: Who Has to Pay Taxes?

In terms of taxes, the United States divides people into two categories: tax residents and non-tax residents. You may be asking how to figure out how immigration and taxes apply to you if you have recently immigrated to the United States?

Even if you are not a US citizen, you may be obligated to pay US taxes in different circumstances. Whether you must file and pay taxes is determined by the government’s classification of you as a tax resident.

However, not all non-immigrant visa holders are tax residents, though. Even if you are not a tax resident, filing an income tax return if you have worked for an employer who withholds taxes from your salary is a good idea since you may be eligible for a refund.

Non-immigrant visa holders can only become tax residents if they stay in the United States for at least 183 days in the current year. For example, if you spend 200 days in the US and have a non-immigrant visa, you must report your earnings to the Internal Revenue Service (IRS).

Furthermore, even if you spent less than 183 days in the United States during the current year, a weighted system could classify you as a tax resident.

Unless you spent less than 30 days in the United States during the current year, you are a tax resident if you have spent at least 183 “weighted” days in the US during the previous 3 years.

This means that if an NRI works in the United States and earns money from India, he is only liable for US taxes. For this purpose, the person must present a US IRS-issued Tax Residency Certificate to his Indian payee. If taxes were deducted in India, the NRI could file a tax claim in the United States for that amount.

NRIs’ income received in India is taxed differently in the United States, depending on their taxation policies. The following are the criteria on which NRI taxation in the United States may be imposed. This can help in tax planning for Indian IT professionals.

1. Income from salary

In India, if an individual receives a pay package with multiple components, each component is taxed separately. Individuals may also qualify for tax breaks or exemptions if they get medical reimbursements or allowances.

In the United States, however, the same taxing conditions do not apply to salaries. An individual’s income is taxed regardless of how much the person earns.

The taxable components of your salary are listed on the well-known Form 16 in India. In contrast, if an individual or NRI files an ITR in the United States, all tax-free components of the pay received in India must be disclosed. At the same time, these individuals must pay taxes on those components in the United States.

NRIs must use the tax return Form 1040 to report their salary income in India. Form 1116 is used to file a tax return or claim a tax credit.

2. Freelancing and contractual income

This is applicable for NRIs who provide consulting services in the United States but earn money from India. In this case, the linked NRIs are taxed in the United States on that income. Therefore, whether the income is received in the United States or an Indian bank account, this tax must be paid.

The provisions of the DTAA, or Double Tax Avoidance Agreement, must be considered in this case.

3. Rental income

If an NRI rents an Indian property, his rental income will be taxed in the United States. Any rental income from immovable property may be taxed in the country where the property is located, according to Article 6 of the DTAA.

As a result, any income from rent in India is subject to taxation for US NRIs. NRIs, on the other hand, must declare this income while submitting their US tax return. Taxes paid in India would be credited to them.

It’s worth noting that salary and contractual income are only taxed in the country where they’re earned. Both countries, however, have the option of taxing rental revenue.

The first right belongs to the country in which the property is located. As a result, the NRI will pay tax on his rental income in India first, according to his available Indian tax slab.

The rental income must then be declared by the NRI taxpayer in the United States. The tax on his entire income is then calculated using his tax bracket in the United States. The NRI might claim a tax credit in the United States for whatever taxes he paid in India.

NRIs in the United States must file Form 1040 Schedule E for tax purposes. In India, rental income is subject to a 30% tax reduction. Actual expenses, such as maintenance and repair, are deducted in the United States. Form 1116 tax credit claims must be completed.

4. Income from the sale of agricultural land

In India, the selling of agricultural land is a tax-free transaction. It is, however, taxed in the United States. An NRI’s income from the sale of agricultural property must be declared in the United States and taxed as part of their global income.

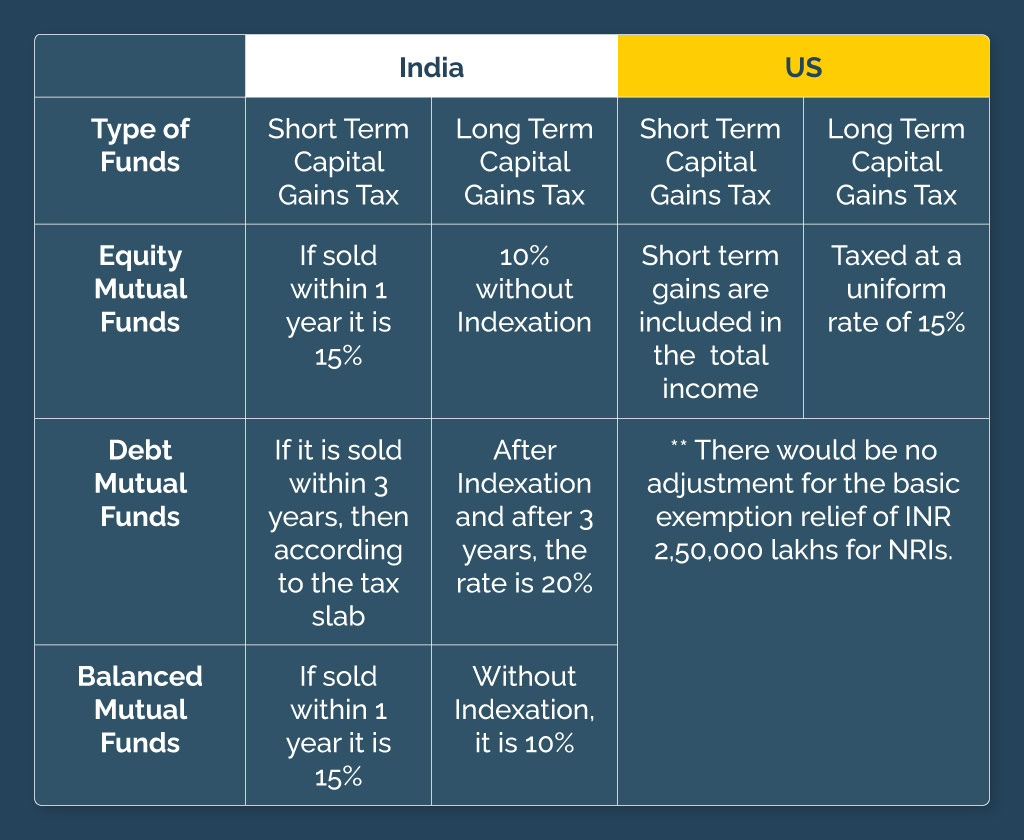

5. Capital gains

A capital gain is any profit earned from selling capital assets such as land, property, stocks, shares, mutual funds, etc. In India and the United States, the time period used to establish whether an asset is a long-term or short-term capital gain is different. NRIs face new challenges because of this.

It may result in NRIs paying tax on their sales in India and additional tax on the remaining amount in the US, notwithstanding the possibility of claiming the tax credit in the US. To an NRI, this could result in a double taxable asset.

Long-term capital gains in the United States are taxed at the same rate for all assets, one year. Long-term capital gains are taxed at a rate of 15%, whereas short-term gains are added to your total income.

The following table summarizes the above topic of capital gains taxes:

6. Income from interest generated

Interest income is added to the total income of each Indian resident and then taxed according to the overall tax bracket. This is usually 30% percent of the interest income.

Interest earned in India or the United States is added to the NRI’s total income and taxed according to the bracket in which it falls. This may be different in the United States, depending on the state’s legislation where the NRI resides.

If an NRI earns interest on deposits in India, he will have a tax deduction of TDS in India at a reduced 15 percent rate if the DTAA is in place.

7. Income from dividends

In India, any dividend income is tax-free. On the other hand, Dividends are added to total income and taxed in the United States.

NRIs must report “Interest and dividends” income on Schedule B of Form 1040 to be taxed. Foreign tax credits can be claimed using Form 1116.

8. Foreign Tax Credit Limit in the USA

In the United States, NRIs can claim a tax credit; however, the IRS has set a limit. For this, you’ll need to fill out Form 1116. This means that the foreign tax credit should be calculated in accordance with the NRI’s US tax due in the same proportion as the NRI’s total income.

It’s important to realize that taxes in the United States differ from state to state. As a result, the taxes paid by NRIs in different states vary. The above criteria for NRI taxation can help in tax planning for Indian IT professionals.

Personal tax returns can be a stressful undertaking. AOTAX can relieve you of this burden by preparing your Personal Tax Returns for you.

We are all Registered Tax Agents with vast hands-on expertise, and we all take great pride in assisting our clients in achieving their objectives.

We do everything we can to minimize your tax while making the overall taxing procedure as efficient, easy, and cost-effective as possible, thanks to a staff of highly skilled and experienced Tax Accountants. Contact us if you are an IT professional working in the USA and looking at filing tax in the USA.

Income Tax Planning for an NRI planning to return to India

Income Tax Planning for an NRI planning to return to India .It might so happen that one fine day you decide to pack your bags and come back home. When you do,there are a few things that Income Tax planning must take special care of. For starters, your investments and tax implications. In general, the tax laws for NRIs returning to the country are fairly generous. However, youmust not be complacent.

A bit of careful planning will ensure that you do not run into any surprises when you come to India, as far as your overseas income and investment are concerned.Tax Resident Status Your tax liability on the income largely depends on your residential status. The FEMA (Foreign Exchange Management Act) and the Income Tax Act govern all these tax rules and regulations. The FEMA keeps a track of all the transactions taking place outside the country for Indian residents. These transactions include foreign bank accounts,money transfers, remittances, lending, gifting, etc. Any investment in real estate or mutual funds is also taken care of by the FEMA. The income tax act on the other hand, looks after the tax liability arising out of such investments. As per the FEMA guidelines, an NRI is someone who currently stays out of India but either is a citizen of India or a person of Indian origin. They must meet either of the following conditions to become a PIO or a person of Indian origin.

– Has held an Indian passport anytime during their lifetime. – Has a spouse of Indian origin. – Was a citizen of India or has grandparents or parents who are Indian citizens.

Foreign Assets The FEMA offers strict and clear guidelines for foreign assets. As per the law, an NRI has the liberty to own, transfer, hold or invest in assets that are outside the country. However, this only comes into the picture if the person bought the asset during their stay abroad or if they have inherited the assets. And not otherwise.

Indian Assets Should a person choose, they can hold on to their Indian assets during their stay in other countries. These include bank accounts, investments, assets etc. however, there are special accounts to hold these. Usually, the two bank account types available for NRIs are FCNR or Foreign Currency Non-Resident and NRE or Non-Resident External Rupee. You can use these accounts to deposit any earnings from outside the country to your local bank accounts.

Income Tax Act The income tax act has clauses with the help of which NRIs can save taxes on their global income for as many as three fiscal years. On coming back to the country, they must convert their NRE or FCNR accounts to RFC accounts. Any interests earned on FCNR and NRE accounts are exempted for NRIs and RNORs.

If an individual was residing in foreign country ordinarily, and brings in money to India, the same is exempted from taxes up to a period of seven consecutive assessment years. The only condition being that the wealth tax exemption is not applicable to income tax and assets which are brought during the stay in India. For NRIs who receive their pension from former employer post moving to India may be taxable. Of course, if there is any double taxation agreement between both the countries, it would govern the taxes. NRIs who are moving back to India permanently, need to consider the above points. Being aware of applicable tax laws and proper planning would ensure a smoother transition phase and allows users to benefit from tax breaks. Since returning NRIs have quite a few tax breaks available for them.

Recent Comments