Types of interest that is eligible for Debt-Tax Deductible

There is a number of debts that would accrue interest on them such as student loans or home mortgage, etc. When the interest accrual is for a longer period, the repayment amount goes on increasing and it turns out to be quite expensive to repay them. If you have several debts then, it is quite obvious for a lot of interest to get accumulated quickly. You might be having low-interest rates but then the only way to pay off is by reducing your outgoing expenses.

Is the interest levied on debt tax-deductible? It might be sometimes; however, it might depend on the type of interest and many other criteria.

Let us find out the types of interest which can be eligible for a tax deduction.

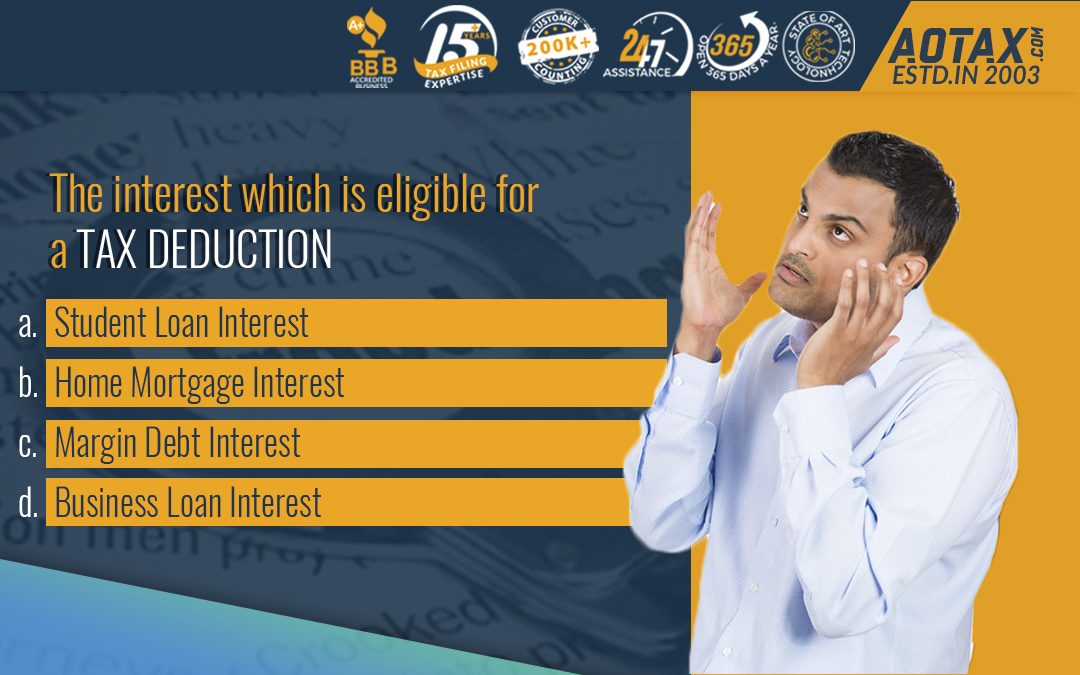

The interest which is eligible for a tax deduction

Student Loan Interest

A large number of the students are under the burden of debts due to the Student loan and to reduce the burden caused by these debts, the IRS provides a tax deduction on the interest which is levied on the Student loan. By the Student loan interest deduction, you can deduct a maximum of $2500 from your income which is taxable as long as the Modified Gross Income (MAGI) of your previous year is less than $70,000. The student loan must be taken either by you, your spouse, or a dependent. The loan must have been taken by you for educational purposes during the period in which you, your spouse, or dependent was enrolled for at least part-time into a degree course.

Home Mortgage Interest

If you are borrowing money for purchasing a home, then you might have the eligibility to avail of the mortgage interest deduction. According to the regulations of the IRS, if you have bought your house after 15th December 2017 you can be eligible to take up to $750,000 in the form of the interest deduction. Moreover, this is also applicable to those mortgages which are up to $1 million and have been purchased before 15th December 2017.

If you are paying home equity loan debt, you can be eligible to take the advantage of the home mortgage interest deduction. However, this is feasible only if you are utilizing the home equity loan for purchasing, constructing, or improving the home which secures your home equity loan.

If you want to claim your interest deduction on a home mortgage, you will require the IRS Form 1098 or the mortgage interest statement which you would obtain from your lender. You would also need proper records that would document the details of your home and mortgage. Moreover, you would obtain the need to obtain the Schedule A too for claiming your itemised deductions. You must carefully read the IRS Publication 936 to get more detailed insight into the types of documentation that the IRS would need to check for your deduction approval.

Margin Debt Interest

In case you are borrowing money from a particular lender for investing, then you would be able to claim a deduction for the interest on the margin debt that has been incurred by you. The value of the deduction is capped at the net taxable income obtained from the investment which you would be able to claim during a tax year; however if you do not have any net taxable income obtained on the investment to claim you can easily carry forward the remaining interest expense. By this, you will have the ability for interest deduction from the net taxable investment income in the next tax-filing year.

The tax deduction for the margin debt interest can be calculated by the use of the IRS Form 4952.

However, you can even calculate the margin interest which is deductible by the below-mentioned steps.

- You consider your gross income and perform subtraction of qualified deductions, net gains, and all other expenses incurred from investment.

- The remaining number obtained is your net investment income.

Let us suppose, you have $1000 as your investment income and $500 as your interest expenses you would be able to deduct $500 on your tax returns obtained.

Business Loan Interest

Business loans would help in providing funds for the expenses incurred in the operation and growth of your business. There are several uses of business loans and can include the accommodation of lines of credit to property mortgages. Business loans also accrue interest over time and this interest accrued is tax-deductible.

The major conditions which determine the tax deductibility of the business loan interest would include the type of business loan you have procured, the relationship between lender-debtor, legal liability for the debt and a proper agreement from both lender and debtor for the debt to be repaid.

Some of the common categories of business loans which would be eligible for small business deductions are:-

- Term loans

- Short-term loans

- Business lines of credit

- Personal loans

- Business Purchase loans

You should use the IRS Form 8990 for calculation of the amount of business interest you can deduct for a particular tax year.

- Sole proprietors and single-member LLCs must claim their deductible interest in the Section –Expenses of Schedule C on Line 16.

- In the case of partnerships and multiple-member LLCs, the expenses related to these interests on business loans can be claimed by recording in Form 1065 and the “Other Deductions” section.

What are the benefits of deducting paid interest?

Your taxable income can be reduced by using the benefit of the interest deduction.

- By taking the advantage of interest deduction, you would be able to move into a lower tax bracket.

- Also, you can be taxed at a lower federal rate by utilizing the benefit of the interest deduction.

Conclusion

Hence, the above-mentioned categories of interest are eligible for the deduction of debt tax and would be beneficial for you to have low taxable income.

Recent Comments