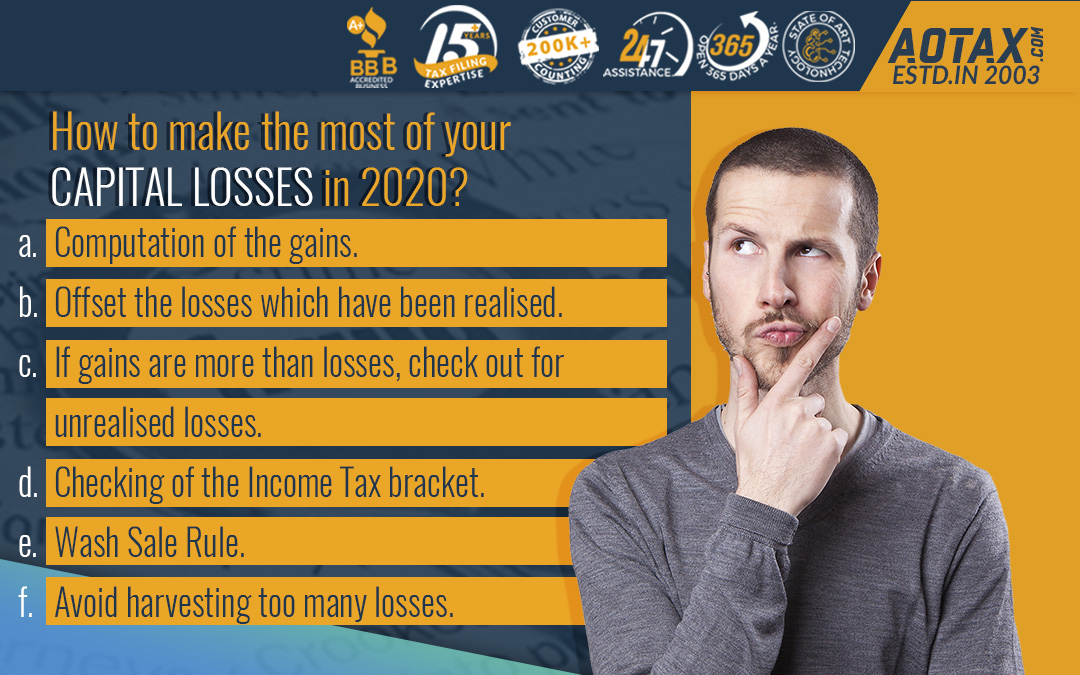

How to make the most of your capital losses in 2020?

How to make the most of your capital losses in 2020?

Capital gains can be said to be the profits that are made when you can sell an investment for more price than at which you have purchased them. On the contrary, if the investments you have made sell at a price which is less than the price at which you bought them is known as Capital Loss.

If you have incurred some capital gains this year and you also have some capital losses in your portfolio, then you can consider the harvesting of these capital losses. By harvesting these losses, you would offset the gains as a result of which you would not have to pay any taxes on the Capital gain income. This process is also termed as Tax-loss harvesting.

Let us check out the process by which you can begin the process of offset of your capital gains by the harvest of capital losses.

Computation of the gains

You should make a list of the sale you have done related to your stocks, bonds, and real estate during the year. You can add the capital fund dividend which you are expecting into your mutual funds.

Offset the losses which have been realized

This would include the various stocks you had purchased when the stock market was high. You even thought or expected the stock market to go higher. However, you had to sell your stocks at a point when the stock market dropped. You also had to sell your stocks at a price that was lower than your purchase price. Moreover, while this process of loss offset you should not forget about the loss carryovers from the previous years. You would be able to find the loss carryovers on Page 2 of the previous year’s Schedule D of your income tax return.

If gains are more than losses, check out for unrealized losses

It might be the scenario that you are holding on to a stock whose prices have dropped. You might be hoping that the prices of the stocks would increase or they will regain their value. You can consider this time as the best time to sell the stock that you have been holding.

Checking of the Income Tax bracket

Before you decide to sell your stock which has dropped in value, you must think about taking some advantages out of the lower capital gain tax rates. For most people, the maximum capital gains rate is around 15%. The rate at which the capital gains are taxed varies according to your taxable income and your filing status i.e. Single, Married and filing jointly, Married and filing separately, Head of the Household.

Wash Sale Rule

The awash sale is said to occur at a point in time when you are either selling or trading securities/stocks at a loss. This wash sale occurs within 30 days of before or after the sale of the securities.

- You can purchase substantially identical securities.

- By a fully taxable trade, you can acquire substantially identical securities.

- Substantially identical securities can be acquired by the use of a contract or option.

If this is done then any loss incurred on the sold assets can be disallowed by the IRS. However, there are a few steps that can be taken to ensure that the capital loss incurred can be used to offset your capital gain.

- You must wait for a minimum of 31 days before you start re-investing into another Stock Fund.

- The next step is to invest in a similar type of fund.

In case, you have disallowed the loss incurred from a wash sale, then you must add up the cost of the disallowed loss into the cost of new securities. This would lead to an increase in the cost of your new stock and also reduce the gains on the sale of the newly purchased stock.

Avoid harvesting too many losses

After you have offset the losses which you have incurred against the gains, the excess losses could reduce up to $3000 of the ordinary income obtained from employment or different other sources. In case, your capital losses are much more than that then the excess losses can be carried over to the upcoming year.

Conclusion

So, these above-mentioned techniques and strategies would help you in making the complete use of capital losses in the year 2020.esting.

Recent Comments